Dell Technologies (NYSE:DELL | DELL Price Prediction) has gone from value-tech afterthought to one of the most consequential AI infrastructure plays in the market, and the chart proves it. The stock is up 227.78% year to date and 245.18% over the past year, yet our model still sees room to run.

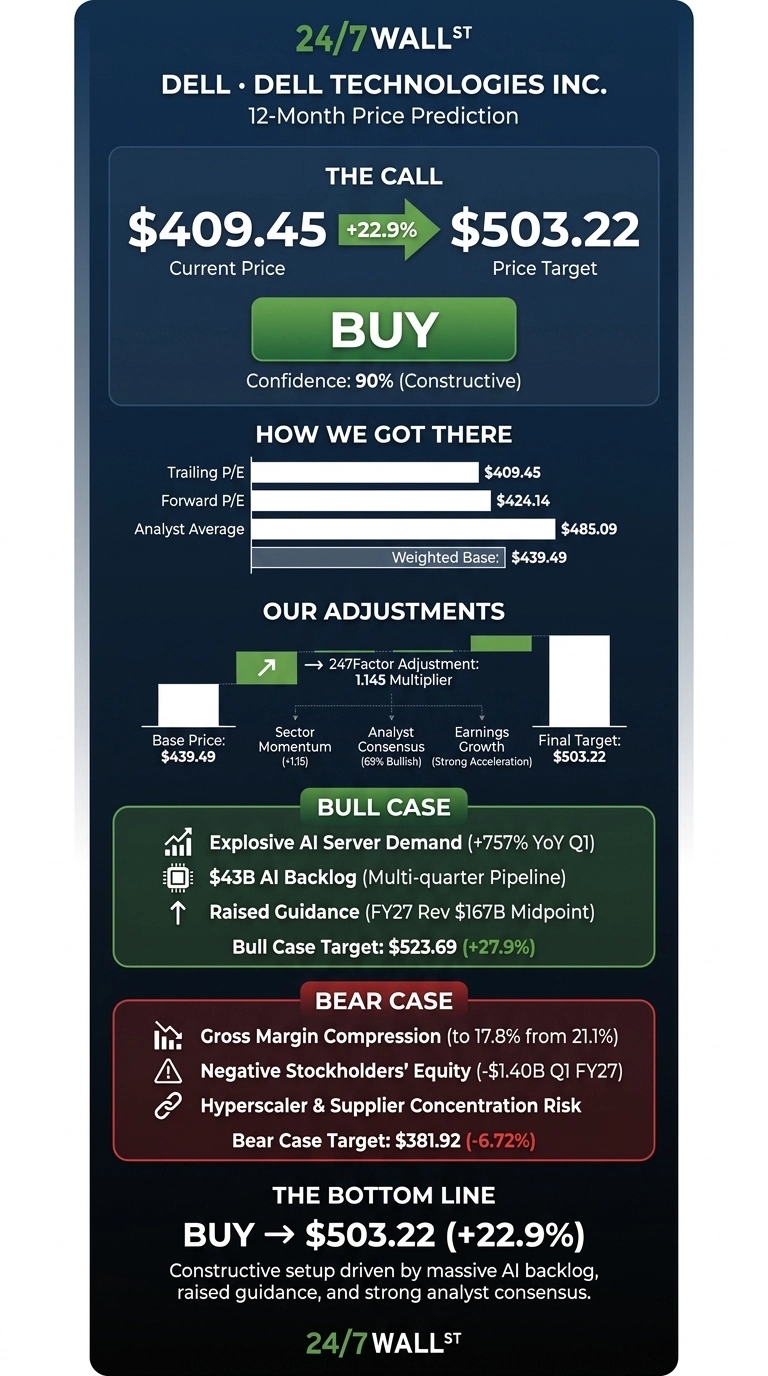

Our 24/7 Wall St. price target for Dell is $503.22, implying 22.9% upside from the current $409.45 price. Our model rates the setup constructively, with a confidence score of 90%. The AI server backlog, raised guidance, and analyst consensus all line up behind the thesis.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $409.45 |

| 24/7 Wall St. Price Target | $503.22 |

| Upside | 22.9% |

| Model Stance | Constructive |

| Confidence Level | 90% |

A Parabolic Run Anchored by a Blowout Quarter

Dell trades just 3% below its 52-week high of $469.47, well above the $109.88 low. Shares climbed 34.21% over the past month after the Q1 FY27 report on May 28, 2026, although the last session cooled 5.67%.

The earnings report was the catalyst. Revenue hit $43.84 billion, up 87.5% YoY, beating estimates by 22.58%. Non-GAAP EPS of $4.86 blew past the $2.96 consensus. AI-optimized server revenue alone grew 757% YoY to $16.13 billion. A reported $1.4 billion Microsoft deal in mid-June added to the momentum.

The Case for $523 and Beyond

The bull case rests on a backlog that keeps refilling. Dell booked $24.4 billion in AI orders in Q1 alone, sitting on a $43 billion AI backlog with a pipeline at multiples of that figure. Management guided FY27 revenue to $165B to $169B and non-GAAP EPS to $17.90 at midpoint, up 74% YoY.

Operating leverage is showing through. ISG operating margin expanded to 10.5% from 9.7%, while CSG widened to 8% from 5.2%. Our bull-case scenario takes shares to $523.69, a 27.9% return. With 18 Buy ratings against just 1 Sell, Wall Street is largely on board.

What Could Go Wrong

The bear case starts with margin compression. Gross margin fell to 17.8% from 21.1% YoY as low-margin AI server mix dominated. Bulls would counter that absolute gross profit still rose 57.6% and operating income climbed 213.8%, so dollars matter more than rates.

Other risks include negative stockholders’ equity of $1.40 billion, NVIDIA single-source supplier dependence, and hyperscaler customer concentration. Competition from Super Micro and HPE remains real. Our bear case scenario lands at $381.92, a 6.72% drawdown.

Putting It All Together

The risk/reward skews constructive at current levels. The 24/7 Wall St. price target of $503.22 reflects a real, fundable thesis built on a $43 billion backlog, raised guidance, and analyst conviction. The setup looks more attractive on any pullback toward the 50-day moving average near $292. The thesis would weaken if AI bookings decelerate sharply or gross margin slips below 17%.

Looking further out, here is where our model projects Dell could trade, assuming current AI infrastructure trends and FCF generation hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $503 |

| 2027 | $575 |

| 2028 | $640 |

| 2029 | $700 |

| 2030 | $758 |

These projections assume Dell continues executing on AI server share gains and storage attach. Significant upside or downside could result from hyperscaler capex shifts or NVIDIA supply timing.

Contact [email protected] for any questions or corrections.