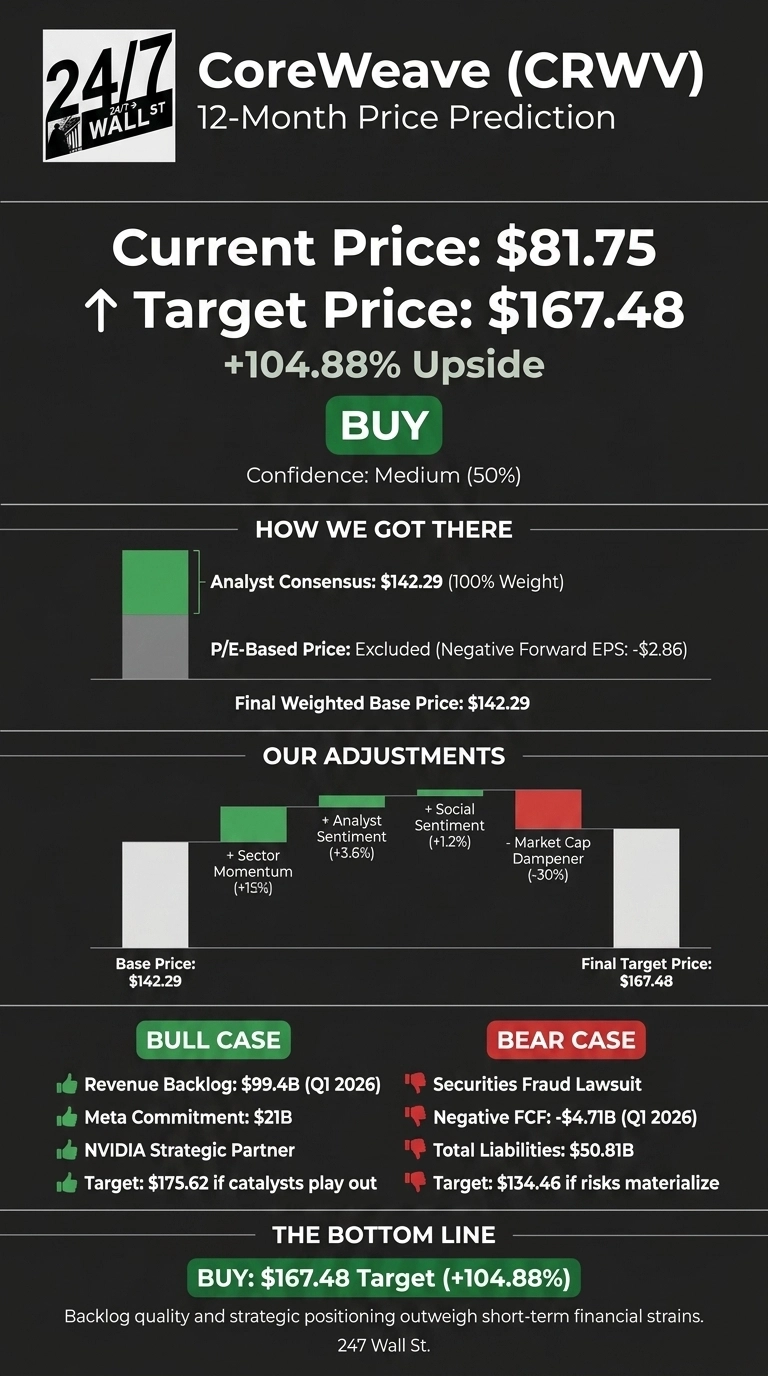

CoreWeave (NASDAQ:CRWV) has been one of the most punished AI infrastructure names of the summer, and I think that has created an opportunity. The stock closed at $81.75 on July 2, 2026, down 31.46% over the past month and 46.14% over the past year.

Our 24/7 Wall St. price target for CoreWeave is $167.48, implying 104.88% upside, and I rate the stock a buy with medium (roughly 50%) confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $81.75 |

| 24/7 Wall St. Price Target | $167.48 |

| Upside | 104.88% |

| Recommendation | BUY |

| Confidence Level | 50% |

How CoreWeave Got Cut in Half

The collapse from $151.77 one year ago to today has been driven by three overlapping narratives. A securities fraud class action alleges CoreWeave concealed data center construction delays and understated reliance on a single third-party data center supplier.

Debt has surged from $2 billion in 2023 to $35 billion, and insiders have been unloading, including CEO Michael Intrator, who sold roughly $37.7 million in shares on June 30, 2026. That backdrop overshadowed a strong Q1 2026: revenue of $2.08 billion, up 111.7% year over year, with a revenue backlog that reached nearly $100 billion after Meta added a $21 billion commitment.

Why Bulls See a Breakout Ahead

The bull case rests on scarcity. CoreWeave has surpassed 1 GW of active power, has contracted more than 3.5 GW, and is targeting 8 GW by 2030. Backlog visibility has gone from $30.1 billion in Q2 2025 to $99.4 billion in Q1 2026. NVIDIA closed a $2 billion Class A stock investment and named CoreWeave its Exemplar Cloud for inference on GB200 NVL72.

Cantor Fitzgerald carries a Buy rating with a $167 target, and Jim Cramer suggested the real backlog may be materially larger than reported. In our upside scenario, CoreWeave reaches $175.62 over 12 months.

What Could Go Wrong

The bear case is real. Q1 2026 free cash flow was -$4.71 billion, capex hit $7.70 billion in a single quarter, and interest expense doubled to $536 million. Total liabilities reached $50.81 billion against $4.76 billion in shareholders’ equity.

It should be noted that bulls would argue the capex spike reflects fulfilling the Meta and OpenAI commitments, and operating cash flow of $2.98 billion plus a $8.5 billion non-recourse investment-grade term loan gives management runway. Still, coordinated insider selling and the securities lawsuit weigh on sentiment. Our bear scenario lands at $134.46 over 12 months.

The Setup: Backlog Quality vs. Balance Sheet Strain

I’m at buy with a 24/7 Wall St. price target of $167.48 and 50% confidence. The factor that tips the scale is backlog quality: $99.4 billion in backlog from customers like Meta, OpenAI, and Anthropic represents committed, contracted demand.

The thesis strengthens if margin expansion accelerates and the securities suit gets contained. The thesis weakens if Q2 2026 shows another double-digit EPS miss or if free cash flow deterioration worsens beyond the current trajectory.

Looking further ahead, here is where our model projects CoreWeave could trade, assuming current growth trajectories and market conditions hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $110.45 |

| 2027 | $167.48 |

| 2028 | $228.59 |

| 2029 | $312.01 |

| 2030 | $425.86 |

These projections assume CoreWeave continues converting its backlog into revenue and progressing toward 8 GW of contracted power. Significant upside or downside could result from AI capex reversal, litigation outcomes, or NVIDIA supply dynamics.

Contact [email protected] for any questions or corrections.