Uber (NYSE:UBER | UBER Price Prediction) now carries a market capitalization of roughly $151.5 billion, backed by a platform that pushed $53.72 billion in Gross Bookings through its apps in a single quarter. Uber has scaled into a $150 billion consumer platform reporting real operating income, and the most recent quarter shows why the market is starting to price it that way.

What It Means

The scale behind the market cap is what makes the profitability turn credible. In Q1 fiscal 2026, reported May 6, 2026, Uber ran 3.6 billion trips across 199 million Monthly Active Platform Consumers, with trips up 20% year over year and audience up 17%. Gross Bookings climbed 25%. Revenue reached $13.203 billion, just missing the $13.263 billion estimate by 0.45%, a gap the company attributes to a roughly 9 percentage-point headwind from business model changes.

The margin story is what pushes this into a new phase. The company’s operating income hit $1.923 billion, up 56.6% year over year. Additionally, adjusted EBITDA margin on Gross Bookings widened to 4.6% from 4.4%, and non-GAAP operating income margin expanded to 3.5% from 3.1%.

Non-GAAP EPS came in at $0.72, beating the $0.7133 estimate and growing 44% year over year, more than double the pace of bookings growth. While GAAP net income of $263 million fell 85.19%, that swing came from a $1.50 billion pre-tax mark on equity investments, with the operating business unaffected.

Market Reaction

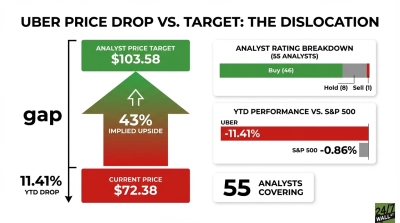

Shares closed at $74.43 on July 2, 2026, up 2.44% on the day and 3.92% over the past month. The year-to-date picture is weaker, with the stock down 8.91% from $81.71 at year-end 2025, and off 19.14% over the trailing year from $92.05. Post-earnings, the stock traded at $77.14 one hour after the filing before settling to $70.71 thirty days later.

Bull Case

I think the bull case around Uber rests on operating leverage that is showing up in every line the market cares about. CEO Dara Khosrowshahi told investors on the call: “Importantly, we’re scaling this growth profitably. Non-GAAP EPS increased 44% year-over-year, more than twice as fast as our bookings growth, driven by disciplined cost management and operating leverage.”

That leverage is being reinforced by a subscription flywheel. Uber One now has 50 million members, up from 30 million at the end of the prior year, growing 50% year on year and driving over 50% of bookings. Members spend 3x more than non-members.

Capital return is now part of the equation. Uber repurchased $3.011 billion of stock in Q1 alone, on top of $6.523 billion in buybacks during full-year 2025. Free cash flow reached $2.286 billion in the quarter, and $9.763 billion for full-year 2025, up 41.6%. The balance sheet backs it up, with debt-to-equity at 0.45, net debt to EBITDA at 0.79, and interest coverage of 12.65. Return on equity sits at 41.37%.

Insiders have been buying into the pullback. CFO Balaji Krishnamurthy and executives Tony West, Jill Hazelbaker, Andrew MacDonald, and Glen Ceremony all acquired shares in June 2026 at a reference price of $73.25, below the April level of $76.48. Analyst sentiment lines up behind Uber, with analyst posting 10 strong buys, 36 buys, 5 holds, and 1 sell, and a target price of $104.53.

Bottom Line

For long-term holders, the $150 billion valuation now sits on top of a business generating margin expansion, buybacks, and a subscription base that is compounding. Uber’s Q2 guidance calls for Gross Bookings of $56.25 billion to $57.75 billion, non-GAAP EPS of $0.78 to $0.82 (growth of 31% to 38%), and adjusted EBITDA of $2.70 billion to $2.80 billion.

Thus, I think the company’s Q2 2026 report is the next reveal. If EPS growth continues to run at more than twice the pace of bookings, the $150 billion platform stops being a ceiling and starts looking like a floor.

Contact [email protected] for any questions or corrections.