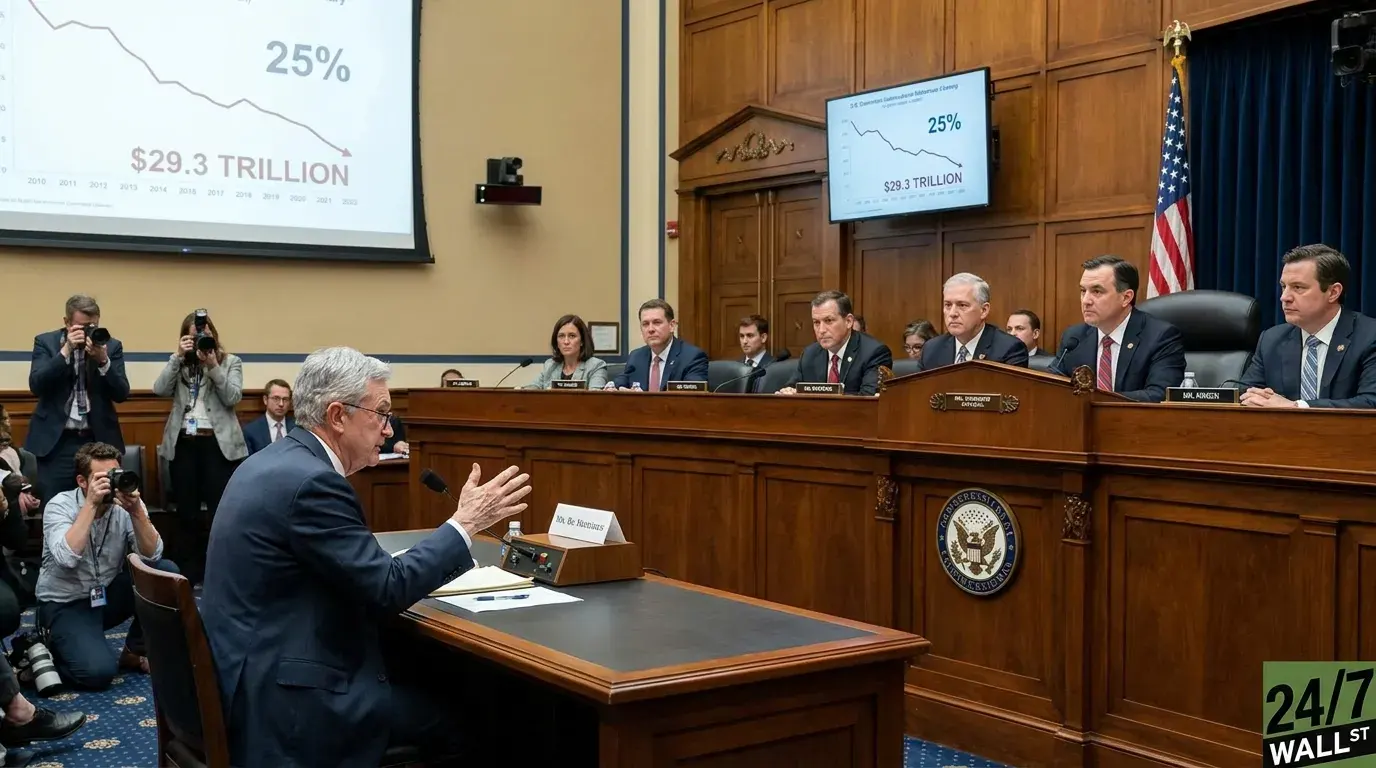

If you opened your phone this morning to a notification claiming Washington wants to slash your Social Security check by a quarter starting next January, you are not alone in feeling a jolt. The figure driving the headlines is real: the 2026 Trustees Report puts the combined Social Security trust funds’ unfunded obligation through 2100 at $29.3 trillion in present-value dollars as of January 1, 2026. That is the gap between every dollar scheduled to go out and every dollar projected to come in over the next 75 years.

Context matters. That number grew from $25.1 trillion in last year’s report, mostly because the actuaries revised down their assumptions for fertility and immigration and added another year to the projection window. For comparison, the entire federal debt sits at roughly $39.3 trillion. The long-run Social Security gap is enormous, but it is a 75-year shortfall measured over decades.

One retiree on a popular forum put it bluntly this week: she is 68, lives on $2,400 a month from Social Security, and wants to know whether she should start hoarding cash now. That instinct is understandable but probably the wrong response.

What the Trustees Actually Said About a 25% Cut

The number behind the scary headline is this: reducing scheduled benefits by 25.2% for all current and future beneficiaries starting in January 2026 would restore 75-year solvency on its own. That is where the “25% benefit cut” line in the news comes from.

What is getting lost in translation is the framing. The Trustees lay out three illustrative, equally weighted options to illustrate the size of the problem for policymakers to weigh. The other two are raising the payroll tax rate from 12.40% to 16.65%, or imposing a steeper 30.3% cut only on people newly becoming eligible in 2026 and after. Most realistic fixes would blend pieces of each.

The report is signed by Treasury Secretary Scott Bessent and HHS Secretary Robert F. Kennedy Jr. in their statutory roles as Trustees, which means they are attesting to the math in their statutory role. Calling this an administration pitch is a stretch.

The Detail That Actually Matters for Your Planning: Time

Here is what retirees should focus on. Waiting makes the menu uglier. The same report shows that if Congress waits until the trust funds deplete in 2034 to act, the equivalent benefit cut grows to 28.5% and the equivalent tax hike grows to 17.30%.

On a $2,000 monthly benefit, a 25.2% cut is roughly $504 a month, or about $6,050 a year. Wait until 2034 and the same cut moves to roughly $570 a month, or about $6,840 a year. That is real money, but it falls within a band of outcomes that policy choices can shape.

Nothing in the 2026 report changes the COLA you already have. The 2026 cost-of-living adjustment is 2.8%, locked in based on third-quarter CPI-W readings. That increase is in your check now.

How This Fits With the Rest of Your Retirement

Social Security is doing heavy lifting in household budgets. In the first quarter of 2026, Social Security paid out $1,630.3 billion, about 32% of all government transfer receipts to households. Meanwhile, the personal savings rate has slipped to 3.9%, the lowest in two years, and consumer sentiment fell to 49.8 in April 2026, recessionary territory.

That backdrop matters because it shapes your buffer. A retiree with a healthy taxable account and a Roth IRA can absorb a hypothetical future benefit trim by adjusting withdrawals. A retiree leaning entirely on Social Security has less room. The right planning move is to look at how much of your monthly need comes from the check versus elsewhere, and stress-test what a 20% to 25% benefit reduction sometime in the next decade would do to your spending plan.

What to Actually Do With This

Two takeaways worth sitting with:

- Do not claim early in a panic. Filing at 62 to “lock in” benefits before a hypothetical cut permanently reduces your monthly check by roughly 30% versus claiming at full retirement age. That is a guaranteed loss to avoid a possible one.

- Build the buffer you can control. A modest cash reserve, careful Roth conversions in low-income years, and a clear picture of your fixed expenses do more than refreshing the news.

Every household’s mix of income, taxes, and time horizon is different, and the policy picture will shift more than once before any of this becomes law. The cost of a thoughtful sit-down with the numbers is a lot lower than the cost of a reactive decision you cannot undo.

Contact [email protected] for any questions or corrections.