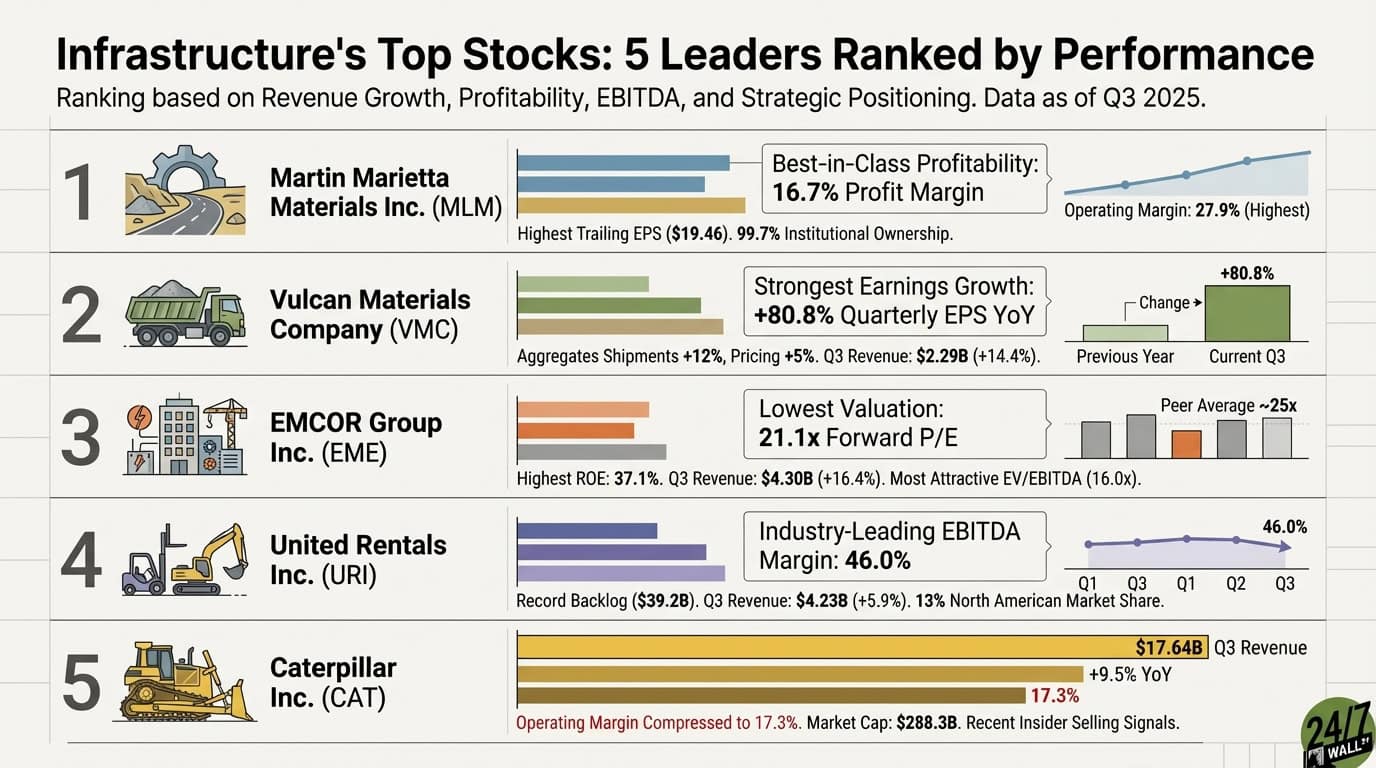

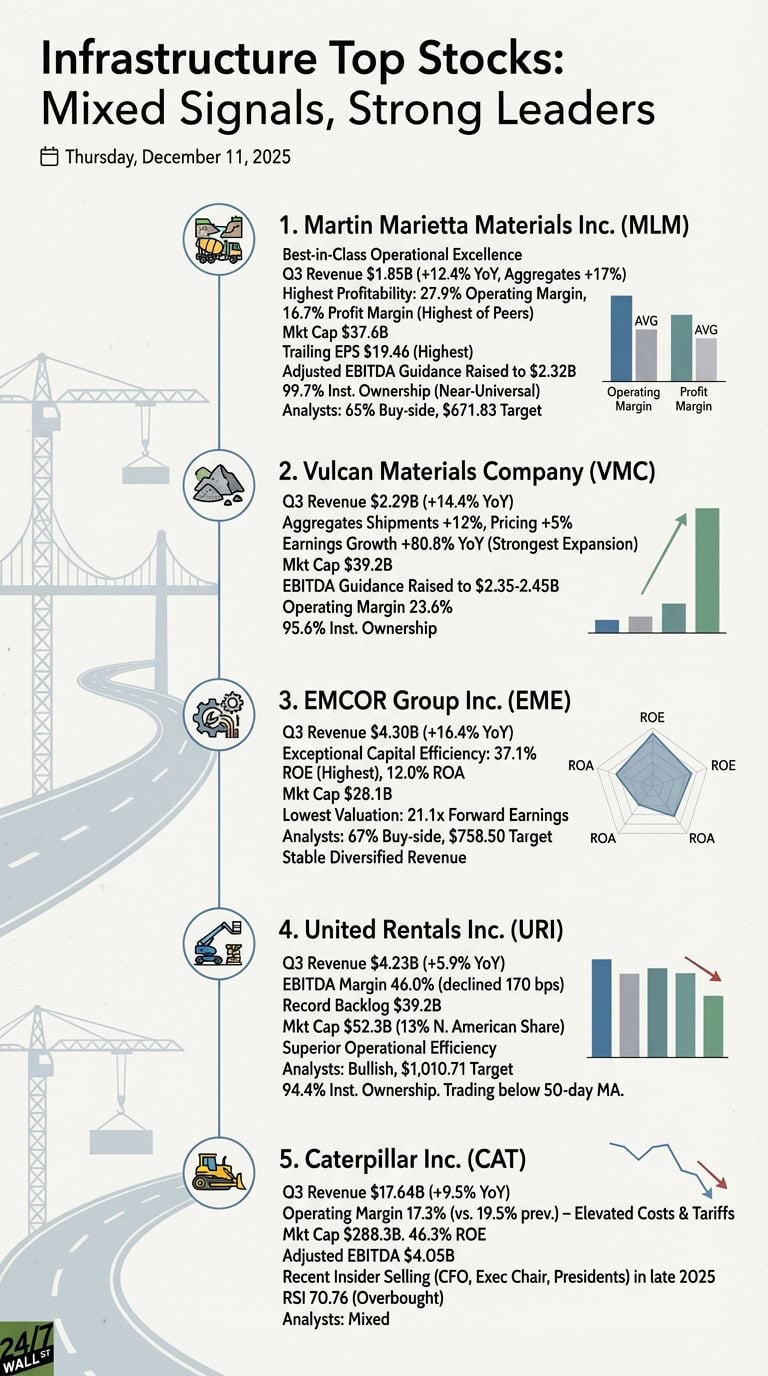

Infrastructure stocks delivered mixed signals in Q3 2025, with companies navigating margin pressures, strong demand dynamics, and varying operational efficiency. This ranking evaluates the sector’s leaders based on revenue growth, profitability margins, EBITDA performance, and strategic positioning heading into 2026.

5. Caterpillar Inc. (CAT)

The world’s largest construction equipment manufacturer generated $17.64 billion in Q3 revenue, marking 9.5% year-over-year growth driven by robust equipment sales. Operating margin compressed from 19.5% to 17.3% due to elevated manufacturing costs and tariff impacts.

With a market capitalization of $288.3 billion, Caterpillar commands a premium valuation at 27x forward earnings and 21.6x EV/EBITDA. The company maintains exceptional return on equity of 46.3% and generated $4.05 billion in adjusted EBITDA during the quarter.

Concerning signals emerged in late November and early December 2025. CFO Andrew Bonfield sold 10,000 shares at prices between $568.57 and $574.52, while Executive Chairman Donald Umpleby III disposed of 2,350 shares. Group Presidents Jason Kaiser and Denise Johnson executed significant stock dispositions at similar price levels.

The stock’s RSI reached 70.76 on December 10, indicating overbought territory near its 52-week high of $617.23. Analyst consensus remains mixed with 14 buy ratings balanced against 14 hold or sell ratings, and the $589.07 target price sits below current trading levels.

4. United Rentals Inc. (URI)

The equipment rental leader posted $4.23 billion in Q3 revenue, up 5.9% year-over-year, while maintaining industry-leading EBITDA margins of 46.0%. Despite strong rental demand contributing to a record $39.2 billion backlog, EBITDA margin declined 170 basis points from the prior year.

United Rentals’ 13% North American market share and $52.3 billion market capitalization position it as the sector’s rental powerhouse. The company delivered $1.95 billion in adjusted EBITDA and returned $1.63 billion to shareholders year-to-date through buybacks and dividends.

At 16.9x forward earnings and 9.1x EV/EBITDA, United Rentals trades at more attractive multiples than equipment manufacturers. Operating margin of 26.5% and profit margin of 15.8% demonstrate superior operational efficiency. Analysts maintain bullish sentiment with 16 buy-side ratings versus seven hold or sell ratings, projecting a $1,010.71 target price that implies significant upside.

The 94.4% institutional ownership reflects strong professional conviction, though the stock currently trades below its 50-day moving average of $885.45.

3. EMCOR Group Inc. (EME)

The mechanical and electrical construction specialist generated $4.30 billion in Q3 revenue, expanding 16.4% year-over-year. EMCOR’s $28.1 billion market capitalization and diversified service offerings across commercial, industrial, and governmental sectors provide stable revenue streams.

EMCOR demonstrates exceptional capital efficiency. Return on equity of 37.1% leads all infrastructure stocks analyzed, while return on assets of 12.0% demonstrates superior asset utilization. The company earned $24.82 in trailing twelve-month earnings per share with a 9.43% operating margin.

Trading at 21.1x forward earnings – the lowest valuation multiple in the group – EMCOR offers compelling value. The 1.73x price-to-sales ratio and 16.0x EV/EBITDA represent the most attractive entry points among peers. Analysts covering the stock maintain 67% buy-side ratings, targeting $758.50.

2. Vulcan Materials Company (VMC)

The nation’s largest aggregates producer delivered exceptional Q3 performance with $2.29 billion in revenue, up 14.4% year-over-year. Aggregates shipments surged 12% while pricing power enabled a 5% increase, driving gross profit up 23%.

Vulcan’s $735 million adjusted EBITDA represented 26.5% growth year-over-year, prompting management to raise full-year EBITDA guidance to $2.35-2.45 billion. Strategic positioning in high-growth Sunbelt markets and favorable weather conditions accelerated construction activity.

Quarterly earnings growth exploded 80.8% year-over-year – the strongest expansion among all infrastructure stocks. Operating margin of 23.6% and profit margin of 14.2% demonstrate pricing discipline in a commoditized business.

At $39.2 billion market capitalization, Vulcan commands a 30x forward earnings multiple, reflecting market confidence in sustained aggregates demand. Institutional ownership of 95.6% and 17 buy ratings from 23 analysts signal professional conviction. The company generated $7.88 billion in trailing revenue with $8.47 in earnings per share.

1. Martin Marietta Materials Inc. (MLM)

The second-largest U.S. aggregates producer claims the top position through best-in-class operational excellence. Martin Marietta generated $1.85 billion in Q3 revenue, growing 12.4% year-over-year, with aggregates revenue specifically expanding 17%.

Martin Marietta delivers industry-leading profitability. Operating margin of 27.9% and profit margin of 16.7% both exceed every competitor analyzed. The company earned $19.46 in trailing earnings per share—the highest in the infrastructure sector—while delivering $6.90 billion in annual revenue.

Management raised adjusted EBITDA guidance to $2.32 billion following record quarterly aggregates performance. The recent Premier Magnesia acquisition strengthens the company’s specialty products portfolio, while strong infrastructure demand across its 26-state footprint provides sustained growth visibility.

Martin Marietta’s $37.6 billion market capitalization trades at 27.9x forward earnings, commanding a premium valuation justified by superior execution. Institutional ownership of 99.7%—the highest in the group—demonstrates near-universal professional ownership. Analysts maintain 65% buy-side ratings with a $671.83 target price, recognizing the company’s operational excellence and strategic positioning for continued infrastructure investment.

Contact [email protected] for any questions or corrections.