Albemarle (NYSE: ALB | ALB Price Prediction) is a global leader in lithium production, supplying battery materials for electric vehicles and grid storage. After a prolonged downturn in lithium pricing, it is also paying dividends while losing money. That tension defines the entire dividend safety question.

Albemarle

| Metric | Value |

|---|---|

| Annual Dividend | $1.62 per share |

| Dividend Yield | ~1.0% |

| Consecutive Years of Increases | 31 years |

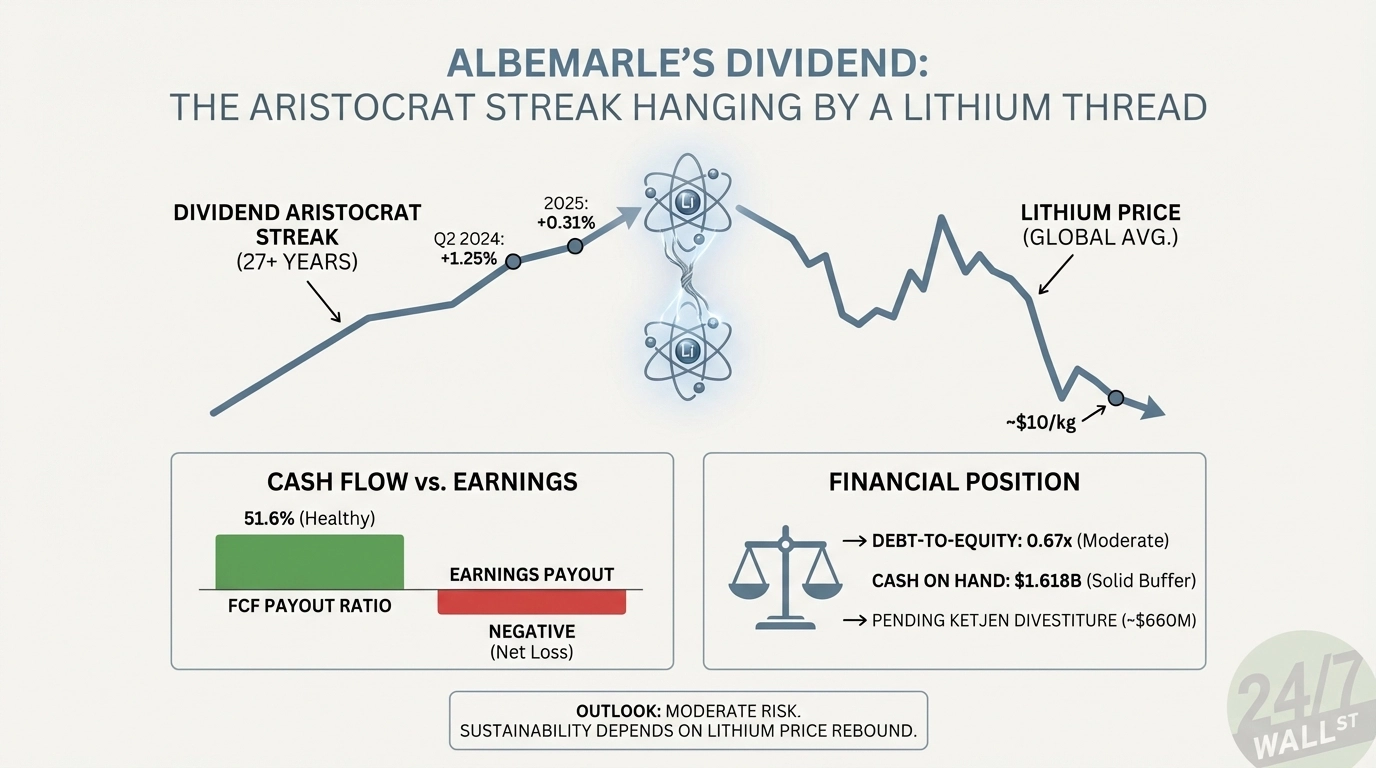

| Most Recent Increase | ~1.25% (Q2 2024) |

| Dividend Aristocrat Status | Yes |

Cash Flow Covers the Dividend. Earnings Do Not.

| Metric | TTM Value | Assessment |

|---|---|---|

| Earnings Payout Ratio | Negative (net loss) | Concerning |

| FCF Payout Ratio | 51.6% | Healthy |

| Operating Cash Flow Coverage | ~3.6x | Strong |

Albemarle paid $357 million in dividends in 2025 against $692 million in free cash flow, a FCF payout ratio of 51.6%. That is genuinely healthy, but context matters: 2024 saw negative FCF of -$993 million, and 2025’s OCF improvement was partly driven by a $212 million inventory reduction that will not repeat. The underlying business posted a net loss of $465 million in 2025.

Debt Is Manageable, but Not Invisible

| Metric | Value | Assessment |

|---|---|---|

| Debt-to-Equity | 0.67x | Moderate |

| Interest Coverage (adjusted) | Near breakeven | Tight |

| Cash on Hand | $1.618B | Solid Buffer |

With $1.618 billion in cash and net debt-to-EBITDA around 1.8x, the balance sheet is not in crisis. The pending Ketjen divestiture, expected to close Q1 2026 for roughly $660 million in gross proceeds, adds flexibility, with management targeting debt reduction as the primary use.

A Streak Preserved by Token Increases

| Year | Annual Dividend | YoY Change |

|---|---|---|

| 2025 | $1.62 | +0.31% |

| 2024 | $1.615 | +1.25% |

| 2023 | $1.60 | +0% |

| 2022 | $1.58 | +0% |

| 2021 | $1.56 | +0% |

The Aristocrat streak is real, but growth has effectively stopped. The five-year CAGR is roughly 1%, with recent increases existing primarily to keep the streak alive. The absolute cost remains low: $357 million annually against $16.4 billion in total assets.

Management Emphasizes Flexibility, Not the Dividend

CEO Kent Masters on Q4 2025 results: “The steps we have taken to optimize our asset portfolio, reduce costs and strengthen our financial flexibility have improved our competitive position.” CFO Neal Sheorey focused similarly on debt: “We are obviously looking at a combination of things, not just gross delevering, but also anything else that we can do with our debt towers.” Neither executive explicitly pledged to protect the dividend. That’s a notable omission for income investors.

Safe for Now, but Lithium Prices Hold the Answer

Dividend Safety Rating: Moderate Risk

The FCF payout ratio of 51.6% is healthy, the cash buffer is substantial, and the absolute dividend cost is low enough to sustain through another difficult year. But earnings are deeply negative, 2025 FCF leaned on non-recurring inventory liquidation, and the recovery thesis depends entirely on lithium prices rebounding from roughly $10 per kilogram. If prices stay depressed, FCF could erode to levels where maintaining even a $357 million annual payout becomes a genuine board-level debate. The streak has survived 31 years. Whether it survives a prolonged lithium bear market depends on a commodity price Albemarle cannot control.

Contact [email protected] for any questions or corrections.