Taiwan manufacturing capacity

Taiwan is the world’s most critical semiconductor manufacturing hub. In 2025 its economy grew by 8.68% and it exported around $550B, growing at a staggering rate of 34% YoY. Electronics traditionally represent around 33% of the total. With the increase in CAPEX by the American and Chinese AI industry, the Taiwanese exports are becoming critical for the whole supply chain.

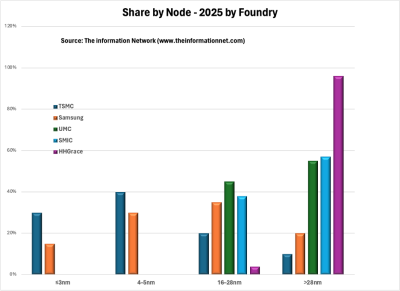

This hyper specialized semiconductor ecosystem is what makes the island so strategically attractive for the leading-edge AI companies and investors alike. No other country combines Taiwan’s semiconductor expertise, equipment and talent on this scale. The evidence is in the numbers, with a 90% global market share for leading-edge chip production.

Taiwan´s industry is deeply integrated, and as the big manufacturers grow, so do the medium and small ones. TSMC ($TSM) might be the most well-known name, as it is also the largest company in Taiwan. The company provides advanced manufacturing services for the fabless chip companies. TSMC is the de facto manufacturing partner for Nvidia, Apple, Google, and leading chip designers. While the company operates fabs in the U.S., Japan, and China, the most advanced fabs with the largest capacity are located in Taiwan.

TSMC and the semiconductor ecosystem

Rising demand for TSMC’s products is forcing its suppliers to scale up in parallel. This creates a multiplier effect across the broader Taiwanese supply chain. As TSMC scales to meet AI demand, hundreds of local suppliers, from wafer polishers to packaging firms like ASE, silicon providers like GlobalWafers, and substrate manufacturers like Unimicron, also do. Virtually all of the big suppliers sit inside EWT and FLTW, which is precisely what makes these ETFs a leveraged bet on Taiwan’s entire AI supply chain, not just its most famous chip maker.

The Taiwanese synergy

Material Suppliers For foundries

Taiwanese industry leaders are deeply intertwined. TSMC, for instance depends on GlobalWafers (6488.TWO), a key silicon wafer supplier, used for chips manufacturing. Globalwafers is the only silicon wafer Taiwanese supplier with a presence in the EWT ETF with a documented relationship with TSMC. In the period of 2018 to 2020, GlobalWafers was one of the 6 main silicon wafer providers used by TSMC to cover 92% of its needs. Moreover, in March 2025 the company further deepened this tie by announcing the co-location of a new manufacturing facility to support TSMC’s Arizona fab.

From Design to Manufacturing

The relationship between MediaTek and TSMC illustrates how deeply intertwined Taiwan’s semiconductor leaders are. Mediatek (2454.TW), Taiwan’s leading fabless chip designer, uses TSMC as their primary foundry. In Q4 2025, Mediatek announced it had adopted TSMC’s 2nm for its next flagship system-on-a-chip (SoC). The chip is expected to enter mass production in the second half of 2026 for use in mobile devices.

The strategic depth of this partnership goes beyond manufacturing. In May 2026, Mediatek CEO Joe Chen reaffirmed TSMC as a key long-term partner. He noted collaboration across nodes from 12nm, down to the next generation of 1.4nm. Moreover, he added the joint work in advanced packaging, optical packaging and Co-packaged optics (CPO).

From Foundry to advanced packaging

The synergy within Taiwan’s semiconductor industry is perhaps most visible between TSMC and ASE Technology Holdings (3711.TW), the world’s largest semiconductor assembler and tester. ASE provides assembly and packaging services, a critical step in delivering finished chips to market.

One of ASE’s highest-margin offerings is Chip-on-Wafer-on-Substrate (CoWoS). The demand for CoWoS is expected to exceed global capacity through 2026. As TSMC’s own packaging capacity runs constrained, OSAT partners like ASE absorb the excess in demand.

TSMC is tying the whole Taiwanese ecosystem.

In 2018, TSMC identified that less than half of the spare parts and raw materials in its Taiwanese facilities were locally sourced. In response to that, TSMC launched the “Parts Localization and Innovation Program” in 2024. The program aims at increasing supply chain resilience and reducing dependence on overseas suppliers. The initiative plans to reach 68% of raw materials and 60% of locally sourced components by 2030.

Early results are already visible, In January 2026, TSMC assisted a Japanese supplier to locally produce electroplating additives to be used in Fab 2,3,5,6, and 8. The company expects that these efforts reduce the production cycle from 60 days to just 20.

TSMC is also deepening the semiconductor ecosystem through supplier development programs. As of February 2026, TSMC collaborated with 12 suppliers to develop 22 Continued Improvement Processes. This signals that the TSMC efforts are also raising the capabilities of Taiwan’s industrial base.

NVIDIA GTC 2026 and Taiwan’s moment

NVIDIA’s CEO, Jensen Huang has expressed in several interviews the relevance of Taiwan for Nvidia and the whole AI ecosystem. At the GTC 2026 he declared ‘Taiwan is the epicenter of the AI revolution. This is where the chips come, packaging comes, this is where the systems are made, this is where AI supercomputers were created. The number of partners we work with here in Taiwan, incredible.’

The company plans to keep expanding its investments in Taiwan, with projections pointing toward $150B per year. That would mean a 10-fold increase since 2021. As those investments materialize, the capital is likely to flow from NVIDIA’s largest suppliers into the whole Taiwanese semiconductor industry.

ETFs to capture the momentum

The Taiwanese industry is so deeply integrated that measuring the AI buildout impact on a single company is nearly impossible, and perhaps unnecessary. For investors seeking broad exposure to Taiwan’s AI momentum, two of the most relevant ETFs are EWT and FLTW.

EWT, launched by Blackrock in June 2000, tracks MSCI Taiwan 25/50 index. A market-cap-weighted index of Taiwanese companies representing approximately 85% of the country’s investable equity market.

FLTW, launched in November 2017, follows the FTSE Taiwan RIC Capped Index. The Index focuses on large- and mid-cap stocks while excluding small-cap firms.

Over the past year, both ETFs have delivered exceptional returns, averaging approximately 90%, due to Taiwan’s exposure to the AI buildout.

Key differences

While both ETFs provide concentrated exposure to Taiwan’s largest companies, they differ on structure and cost. EWT, with $10.5B in AUM is larger than FLTW $2.8B. The gap directly translates to tighter spreads and higher daily trading volume. For EWT the volume is around 5.8M versus 1M for FLTW. For active traders the liquidity difference could be meaningful.

However, for long-term investors, FLTW makes a compelling case. Its expense ratio of 0.19% versus 0.59% may seem minor, but on a $100K investment over 20 years that 0.40% annual gap compounds to $30K. Not only that, the 5 year annualized return for FLTW is higher at 21.2%, versus 18.0% for EWT. On top of that, the broader diversification of FLTW with 135 positions compared to just 87 from EWT.

Despite the differences, both ETFs share the same top positions : TSMC, Mediatek, Delta Electronics, Hon Hai Precision and ASE technology. Moreover, both ETFs have delivered near-identical YTD returns in 2026, approximately 68%.

Risks

These ETFs carry at least four key risks worth acknowledging: the geopolitical tension, the susceptibility to natural disasters on Taiwan, the heavy concentration in TSMC (20% of both funds) and dependence on the AI CapEx cycle .

Geopolitical risk remains the most difficult to quantify. Any conflict materialization would be catastrophic for both ETFs.

Taiwan is prone to natural disasters. The island experiences approximately 2000 earthquakes per year, 200 being perceptible. In April 2024 a 7.2 magnitude earthquake caused $92M in losses for TSMC alone, reducing Q2 2024 gross margins by 0.5 percentage points.

Finally a heavy concentration in TSMC and a potential slowdown in AI CapEx spending, would likely produce a selloff in both ETFs.

Valuation framework

After one of the strongest rallies in either ETFs historic performance, the question is whether the market has already priced the best-case outcome. The following framework uses earnings data to estimate current valuations and identify what needs to happen before adding exposure.

AI revenue exposure, gross margin and total revenue

|

Company |

EWT weight |

FLTW weight |

Gross Margin Q1’26 |

AI revenue Share |

Q1’26 revenue |

AI revenue Q1’26 |

|

TSMC |

20.7% |

19.9% |

66.2% |

61% |

$35.9B |

$21.9B |

|

Delta Electronics |

5.1% |

6.4% |

37.0% |

30% |

$5.0B |

$1.5B |

|

Mediatek |

6.3% |

5.2% |

46.0% |

5% |

$4.7B |

$0.75B |

|

ASE technology |

2.6% |

2.4% |

20.1% |

15% |

$5.5B |

$0.8B |

|

Hon Hai |

3.9% |

5.5% |

6.2% |

48% |

$66.6B |

$32B |

AI revenue exposure, gross margin & total revenue — top 5 shared holdings . Note: HonHai cloud & networking segment includes AI servers

TSMC guidance full-year 2026 revenue growth above 30%. The combined confirmed AI-related revenue across the largest five shared holdings yields an estimated $228B annualized. This represents just a fraction of the ETF’s total annualized revenue, and better captures the exposure to the AI Infrastructure buildout.

Valuation scenarios

In December 2025, EWT traded at 20x earnings. By Q1 2026, the valuation expanded to 31.8x, 59% appreciation in just one quarter. The market is already pricing a revenue surge.

|

Case |

Bull case |

Base case |

Bear case |

|

Earnings growth |

+35% |

+25% |

+15% |

|

Implied fair P/E |

28-32x |

22-25x |

16-18x |

|

Hyperscaler CapEx |

+$670B |

+$600B |

+$500B |

|

PEG |

0.91 |

1.27 |

2.12 |

At 31.8x earnings, the ETFs are already pricing in the bull case. Under the base case of 25% earnings growth, the PEG ratio climbs to 1.27. This implies that the ETFs are trading 20% above the fair value. A deceleration to just 15% growth would imply 35-40% downside. The key variable across all three scenarios is whether TSMC’s 30% growth guidance holds through the year, which is tied to the hyperscaler CapEx commitments above $670B holding true for the second half of 2026.

Conditions that would change the entry case

The most direct input into the bull case is whether the four major hyperscalers maintain or raise their combined CapEx commitments above $670B. Delta electronics CFO cited the figure on Q1 2026 as the determining factor behind the company’s record margins. If the spending holds or increases, TSMC’s own 30% growth guidance embedded within the current P/E is plausible. If the spending is reduced, the base case of 1.27 becomes more probable.

Second, TSMC gross margin is a good indicator to hold the bull case intact. The company reported 66.2% in Q1’26 and guided for Q2 65.5%-67.5%. A result in that range would signal the narrative is maintained, while a result below 62%, Q4 ’25 level, would suggest guidance predictions are overestimating and the growth story might lag.

Third, a degradation of the P/E to historical range, from 22-25x would represent a materially better entry point. At 22x EWT would trade near $70, at 25x near $80. In that range, with the bull case intact, the PEG would drop to 0.72-0.83, making the entry case compelling.

A fourth condition is less predictable but worth monitoring. In March 2026, Elon Musk announced Terafab. An ambitious project to build Tesla and SpaceX’s own chip fabrication facility. Musk chose Intel’s 14A process over TSMC. If Terafab struggles to execute, the most likely scenario would reinforce TSMC’s irreplaceability and drive additional demand back to Taiwan’s ecosystem.

The Takeaway

At current levels, both ETFs are priced for perfect execution. For investors already holding positions, the framework suggests monitoring TSMC gross margin and revenue during Q2 2026. For investors considering initiating a position, the $70-80 range on EWT represents an attractive level.

Authors opinion

Taiwan is the world’s most critical semiconductor manufacturing hub and indispensable for the AI supply chains. Last year its economy grew at a staggering rate of 8.68% and its exports surged 34%. The momentum shows no signs of slowing as hyperscalers deepen their commitments to the island. Nvidia alone has announced plans to spend $150B per year in Taiwan.

TSMC’s initiatives aim to further integrate the ecosystem, to reduce costs, environmental impact and increase resilience to geopolitical factors.

For investors, EWT and FLTW offer two efficient entry points into Taiwan’s semiconductor manufacturing momentum. The thesis is intact, as the AI buildout continues, Taiwan’s ecosystem is structurally positioned to capture a disproportionate share of that growth. Nonetheless, At 31.8x earnings, both ETFs are pricing in perfect execution. Watch TSMC’s Q2 gross margin and hyperscaler CapEx guidance: if either disappoints, the $70–80 range on EWT becomes the entry point where conviction and price finally align.

Contact [email protected] for any questions or corrections.