Income investors who built their portfolios entirely around U.S. dividend payers are leaving yield on the table in 2026. Three international dividend ETFs, Vanguard International High Dividend Yield Index Fund (NASDAQ:VYMI), iShares International Select Dividend ETF (NASDAQ:IDV), and Schwab International Dividend Equity ETF (NYSEARCA:SCHY), now distribute meaningfully more income than the benchmark Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) many income portfolios are anchored to.

The gap is structural. European and Asian large caps trade at about half the price/earnings multiple of the U.S. market in some cases, and overseas companies have long paid out a larger share of earnings as dividends rather than buybacks. Layered on top: a soft dollar backdrop that Franklin Templeton expects to persist through 2026, which converts foreign distributions into more dollars for U.S. holders. Each fund below earns its place through a distinct mechanism, and they are not interchangeable.

Why the yield gap exists in 2026

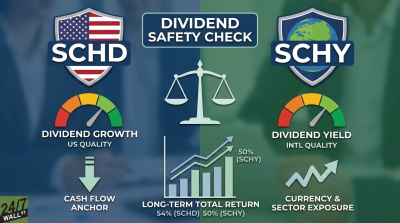

SCHD currently yields roughly 3.9% on a trailing basis, sitting on $71.6 billion in assets and a portfolio led by Bristol-Myers Squibb, Merck, ConocoPhillips, Lockheed Martin, and Chevron at roughly 4% weights each. It is a quality-screened U.S. dividend machine. The case is for pairing it with international exposure.

International equities currently trade at a wide valuation discount to the S&P 500, and Morningstar flags Denmark, the Netherlands, Germany, France, and the UK as the most undervalued developed pockets. Cheaper starting multiples mean higher starting yields. Add a payout culture in Europe and Australia that favors cash dividends over share repurchases, and the income premium becomes durable rather than cyclical. The tradeoffs are real: currency swings can move quarterly distributions in dollar terms, and foreign withholding taxes apply, though most are recoverable through the foreign tax credit in taxable accounts.

VYMI: the broadest passive net

Vanguard’s international high-yield fund is the simplest building block. It tracks the FTSE All-World ex US High Dividend Yield Index, which captures large- and mid-cap dividend payers across both developed and emerging markets. That ex-US scope is the differentiator: VYMI is the only fund on this list with meaningful exposure to Taiwan, China, India, and Brazil, alongside core European and Japanese names.

The current SEC yield sits at 4.2%, and the expense ratio of 0.07% is the lowest in the international dividend category. The fund manages $13.05 billion, which gives it tight bid/ask spreads and deep liquidity for institutional flows.

Total return has kept pace with the income story. VYMI has gained about 10% year to date and nearly 28% over the trailing year, with shares around $99. The catch with VYMI is the same as its strength: emerging-market exposure adds currency and geopolitical volatility that pure developed-markets funds avoid. For investors who want one fund to cover the entire ex-US dividend universe at the cheapest possible cost, this is the default answer.

IDV: the concentrated yield play

IDV is the option for investors who want the maximum dividend income an ETF wrapper can extract from international markets, and who understand they are accepting concentration risk to get it. The fund tracks the Dow Jones EPAC Select Dividend Index, which screens developed markets outside North America for the highest-yielding stocks that also meet dividend-quality filters. The result is a portfolio heavily tilted toward financials, utilities, and consumer goods, with country weights concentrated in the UK, Australia, France, Italy, and Spain.

The trailing 12-month yield runs in the 5% to 6% range, the highest of any fund discussed here. That income premium comes with the cost structure: at 0.50%, the expense ratio is materially higher than VYMI’s, and the sector concentration means a banking crisis in Europe or a regulatory hit to UK utilities can drag returns more than a broadly diversified peer would suffer.

Performance has rewarded holders so far. IDV is up about 11% year to date and nearly 34% over the past year, with the highest one-year total return on this list. Think of IDV as a higher-octane income engine, useful when an investor’s primary goal is current cash yield and the rest of the portfolio already provides diversification.

SCHY: the overlooked quality cousin

SCHY is the contrarian inclusion here, and for SCHD holders it should be the first stop. Schwab built it as the international sibling to SCHD, applying the same Dow Jones methodology that drives the U.S. flagship to a screened universe of international payers. The fund tracks the Dow Jones International Dividend 100 Index, which requires 10 consecutive years of dividend payments and ranks survivors on cash flow to debt, return on equity, dividend yield, and five-year dividend growth.

That quality filter is the entire point. Funds chasing only the highest yields tend to load up on stretched payers right before cuts. SCHY’s screen is engineered to weed those names out, which is why its trailing yield of roughly 4% sits below IDV’s even though both pull from similar geographies. Investors get a methodology familiar from their U.S. holdings, applied to a cheaper, higher-yielding foreign market.

The tradeoff is shorter operating history relative to IDV, which launched in 2007, and lower yield than the pure income plays. For SCHD owners specifically, SCHY is the cleanest mental model: same rules, different passport.

Picking between the three

The decision rests on what an all-domestic income investor is trying to accomplish. VYMI is the right choice for the investor who wants one ticker, the lowest possible cost, and exposure to emerging markets alongside developed peers. It is the closest international analogue to owning a broad U.S. total-market dividend fund.

IDV fits the investor whose mandate is cash income, who already has growth exposure elsewhere, and who can tolerate sector concentration in European banks and utilities. The yield premium is real, and so is the risk that a single sector shock hits harder than it would in a diversified peer.

SCHY is the answer for SCHD loyalists who want their international sleeve to behave the same way their domestic sleeve does. The quality screen sacrifices some headline yield in exchange for fewer dividend cuts and a methodology the investor already trusts. All three funds sit alongside SCHD, adding income and geographic diversification that a U.S.-only portfolio structurally cannot produce.

Contact [email protected] for any questions or corrections.