Disney (NYSE:DIS | DIS Price Prediction) has spent 2026 grinding sideways while the underlying business quietly accelerates. Shares are down 10.98% year to date, yet streaming margins just crossed double digits and FY26 EPS growth is guided at roughly 16%. That disconnect is the entire setup for our call.

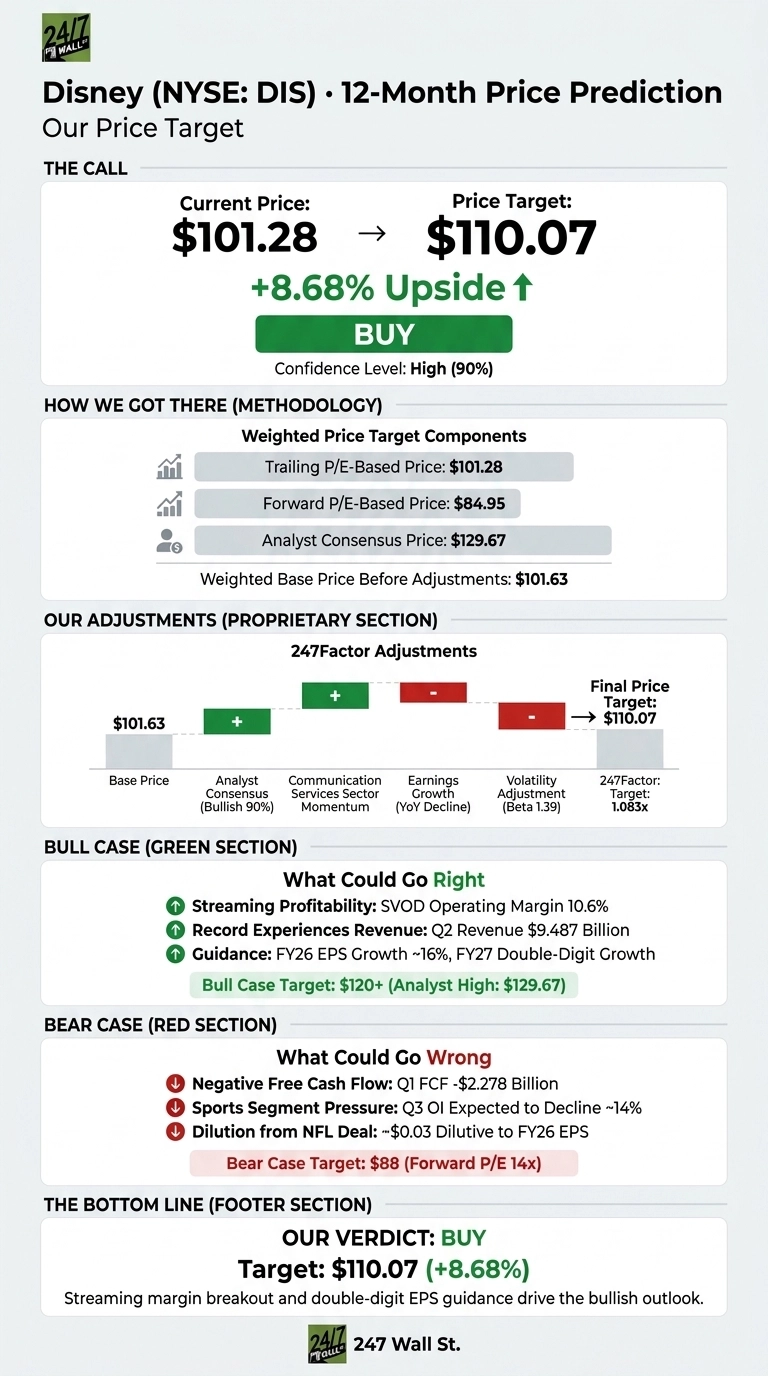

Our 24/7 Wall St. price target for Disney is $110.07, implying 8.68% upside from $101.28. We rate Disney a buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $101.28 |

| 24/7 Wall St. Price Target | $110.07 |

| Upside | 8.68% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Streaming Inflection Hiding Behind a Sideways Tape

Disney is down 14.3% over the past year and up 1.96% over the past week, with a 14-day RSI of 49.03 that reads as neutral. The stock sits between a 52-week low of $92.19 and a high of $123.85.

The May 6 earnings report told a much better story than the tape. Q2 FY26 adjusted EPS came in at $1.57 versus $1.4955 expected, on revenue of $25.168 billion, up 6.55% year over year. Operating income jumped 31.29%, Entertainment SVOD operating income surged 88% to $582M, and the Experiences segment posted record Q2 revenue of $9.487 billion. Management raised the buyback target to at least $8 billion.

The Case for $120+

The bull thesis hinges on streaming. Entertainment SVOD just hit a 10.6% operating margin, with 196M combined Disney+ and Hulu subscribers. Add the ESPN DTC launch, the NFL Network acquisition, and double-digit FY27 EPS growth guidance, and the operating leverage story is real.

Experiences keep printing records, helped by recreation spending of $864.2 billion in April 2026, a fresh high. The $129.67 analyst target, backed by 27 Buy ratings versus 1 Sell, is the bull scenario. Hit FY27 EPS estimates with a 19x multiple and Disney trades north of $120.

What Could Go Wrong

Q1 FY26 free cash flow swung to negative $2.278 billion on California wildfire tax payments, and Q3 Sports operating income is guided down roughly 14% on higher programming costs. The NFL deal is $0.03 dilutive to FY26 EPS, and Polymarket traders give Disney+ only a 28% chance of reaching 150M users by September.

Bulls would counter that the Q1 cash flow hole reflected tax timing rather than operational weakness, and that Q2’s $4.941 billion in free cash flow shows the underlying engine is intact. A bear scenario clipping the multiple to 14x forward earnings drags the stock toward $88.

Disney Price Prediction 2026-2030

The 24/7 Wall St. price target of $110.07 is a buy with 90% confidence. The tipping factor is the SVOD margin breakout combined with a forward P/E of just 14x on a name guided to 12% to 16% EPS growth. The setup favors investors who believe streaming margins keep expanding into FY27. Investors who think Sports rights inflation eats the entire DTC win may want to wait for further evidence.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $110 |

| 2027 | $122 |

| 2028 | $135 |

| 2029 | $148 |

| 2030 | $162 |

These projections assume Disney executes on the double-digit EPS growth path guided for FY26 and FY27. Material upside or downside hinges on streaming margin trajectory, NFL economics, and the pace of Experiences expansion in Asia and the Middle East.