My buy order on Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has fired five times this year, and the sixth sits queued for Monday morning. The stock is down. The headlines are nervous. I keep adding, and I am writing this to explain exactly why.

What pulls me back is simple. Microsoft sits at the center of the agentic computing era with the balance sheet, the contracted customers, and the cash flow to fund the buildout without flinching. Satya Nadella runs it like an owner. The numbers behind that sentence are the reason I cannot stop hitting buy.

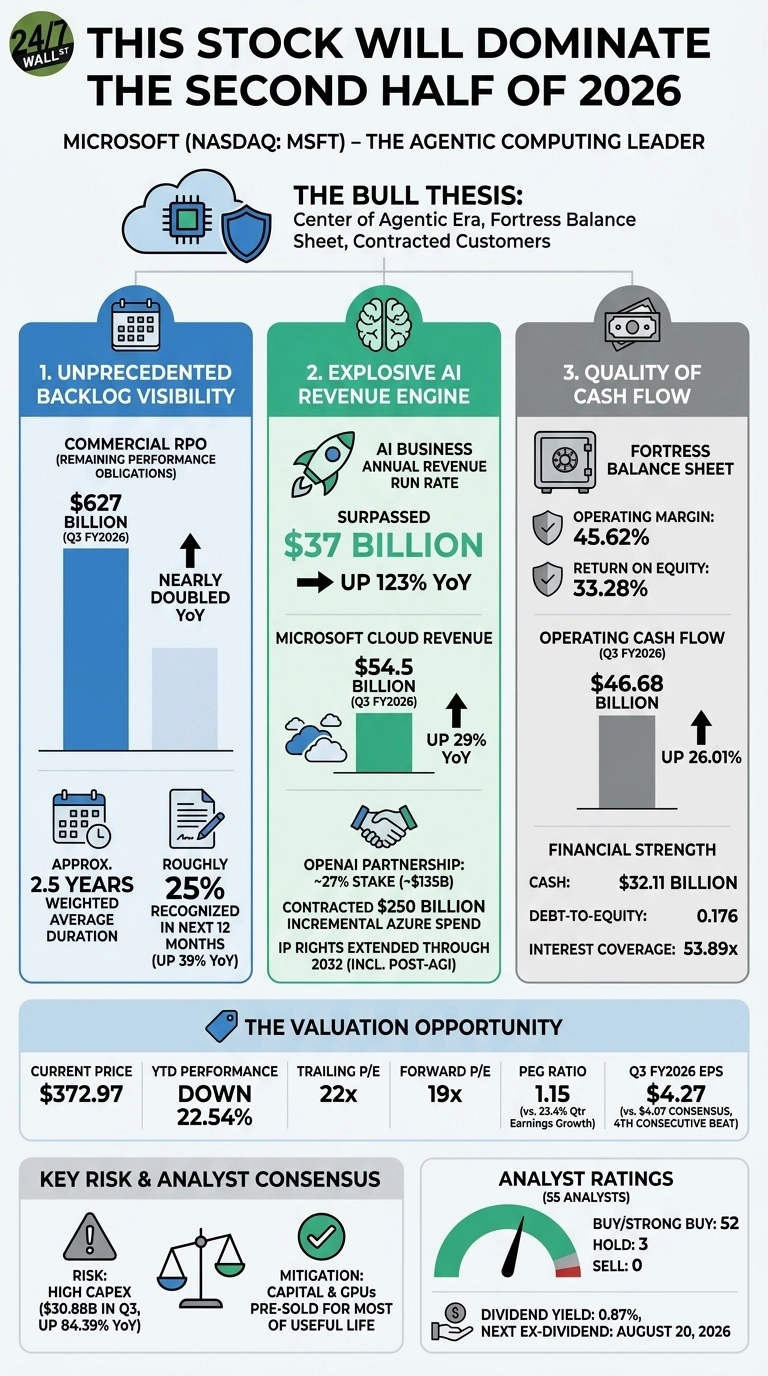

The Backlog Tells Me What Happens Next

Reason one is contracted revenue. Commercial remaining performance obligations reached $627 billion in Q3 FY2026, a figure that nearly doubled year over year. CFO Amy Hood noted weighted average duration of approximately two and a half years, with roughly 25% recognized in revenue in the next twelve months, up 39% year over year. That is multi-year visibility most companies would trade a kidney for.

Reason two is the AI engine. The AI business crossed an annual revenue run rate of $37 billion, up 123% year-over-year. Azure grew 40%. Microsoft Cloud revenue hit $54.5 billion, up 29%. The restructured OpenAI partnership carries Microsoft’s stake at roughly 27%, worth around $135 billion, plus a contracted $250 billion of incremental Azure spend and IP rights extended through 2032, including post-AGI models.

Reason three is the quality of the cash. Operating margin sits at 45.62%. Return on equity is 33.28%. Operating cash flow in Q3 alone was $46.68 billion, up 26.01%. The balance sheet holds $32.11 billion in cash against debt-to-equity of 0.176 and interest coverage of 53.89x. This is a fortress paying for its own growth.

The Valuation I Am Buying Into

Price did the work for me. Shares closed at $372.97, down 22.54% year to date. Forward P/E sits at 19x. Trailing P/E is 22x. PEG is 1.15 against quarterly earnings growth of 23.4%. EPS came in at $4.27 versus $4.07 consensus, the fourth straight beat. I am paying a reasonable multiple for a business compounding earnings in the low twenties.

The Risk I Will Not Pretend Away

Capex hit $30.88 billion in one quarter, up 84.39% year over year. If AI demand softens before this infrastructure earns its return, margins compress and the bear case lands hard. OpenAI investment losses already swung to $3.1 billion in Q1 FY2026 versus $523 million a year earlier. Reddit’s loudest bears called it capital incineration in a thread titled “Satya and Zuckerberg are incinerating capital” that drew over a thousand upvotes.

I read that thread. Then I read Amy Hood’s reminder that much of the capital we’re spending today and the GPUs we’re buying are already contracted for most of their useful life. The capex is pre-sold. That changes the calculus, and it is why the buildout does not scare me out of the position.

Why The Buy Button Stays Live

The dividend yield is modest at 0.87%, with the next ex-dividend date on August 20, 2026. The payout is a bonus.

I own this stock because contracted revenue, cloud growth, and pricing power are compounding through one of the largest infrastructure transitions in software history. Of 55 analysts covering the name, 52 rate it buy or strong buy with zero sells. I am buying alongside them, and I will keep buying until the thesis breaks.

Contact [email protected] for any questions or corrections.