With Netflix (NASDAQ:NFLX | NFLX Price Prediction) reporting Q2 2026 earnings on July 16, the stock is at a crossroads. Shares trade at $77.65, down 39.57% over the past year, yet the streaming leader raised full-year free cash flow guidance to roughly $12.5 billion.

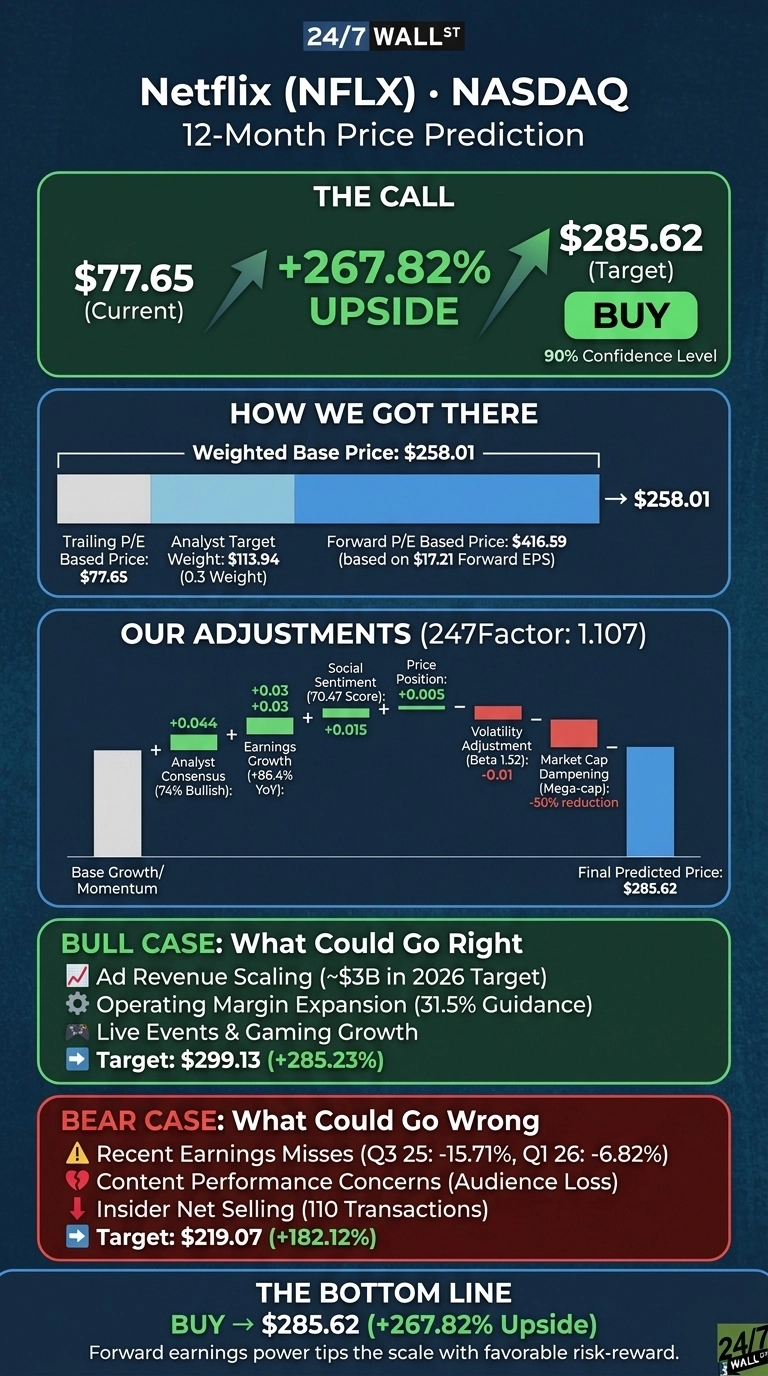

Our 24/7 Wall St. price target for Netflix is $285.62, implying 267.82% upside over the next 12 months. Our model rates the setup buy with a confidence level of 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $77.65 |

| 24/7 Wall St. Price Target | $285.62 |

| Upside | 267.82% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Year, A Different Setup

Netflix shares fell nearly in half from the $129.50 52-week high, bottoming at $70.86 before recovering. Year-to-date, NFLX is down 17.18%, though it rose 9.52% last week on news of an AI advertising partnership with Omnicom Media Group.

Q1 2026 revenue landed at $12.25 billion, up 16.2% year over year, with EPS of $1.23 against a $1.32 estimate. Net income surged 82.77%, inflated by a $2.8 billion Warner Bros. termination fee. Free cash flow jumped 91.44% to $5.09 billion. Management reaffirmed FY revenue guidance of $50.7 billion to $51.7 billion and Q2 revenue guidance of $12.574 billion.

The Case for $299 and Higher

Bulls point to a widening moat in monetization. Ad revenue is tracking toward roughly $3 billion in 2026, double the prior year, and ad-supported tiers now drive more than 60% of sign-ups in ad markets. Advertiser count jumped 70% YoY to 4,000-plus clients.

Operating margin guidance stepped up to 31.5%, with Q2 targeting 32.6%. Live events (Tyson Fury vs. Anthony Joshua, MLB, NFL), gaming, and international expansion at under 45% global broadband penetration extend the runway.

Our bull case scenario points to $299.13, and the Wall Street consensus target of $113.94 implies healthy near-term upside from 37 Buy and Strong Buy ratings against 13 Holds and zero Sells.

What Could Go Wrong

NFLX missed on the bottom line in two of the last four quarters, including a 15.71% miss in Q3 2025 and a 6.82% miss in Q1 2026. Historically, Netflix misses trigger a 9.89% single-day drop. Reddit sentiment cratered from 82 to 28 in the past week on concerns that top shows are losing 30% to 70% of their audience between seasons.

Insider activity has been net selling across 110 recent transactions. Polymarket traders assign only a 6.6% probability of NFLX reaching $100 probability in July.

The Q1 EPS miss reflects heavy content amortization that management says peaks in Q2 before decelerating. The Brazilian tax charge of roughly $619 million that hit Q3 2025 was non-recurring. Bear case downside from our model points to $219.07, still well above the current price.

What to Watch Into Earnings

The 24/7 Wall St. price target sits at $285.62 with 90% confidence and a buy rating. Forward earnings power tips the scale. With forward EPS of $17.21 against a trailing P/E of 25, the risk-reward skews sharply positive after the 39.57% drawdown.

The setup strengthens if the July 16 report reaffirms the $12.5 billion free cash flow guide and shows ad revenue on pace to double. The thesis weakens if operating margin slips below 31.5% or if subscriber growth in APAC and LATAM decelerates from Q1’s 20% and 19% pace.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $134.04 |

| 2027 | $285.62 |

| 2028 | N/A |

| 2029 | N/A |

| 2030 | N/A |

These projections assume Netflix executes on ad-tier scaling, live events, and international penetration, with our 5-year base case pointing to $3,369.45 by July 2031. Downside could result from content amortization pressure, FX volatility, or competitive escalation from Alphabet, Amazon, Disney, or TikTok.

Contact [email protected] for any questions or corrections.