The Northwestern Mutual 2025 Planning & Progress Study put a clean number on something Americans have been hinting at for years: 40% of adults expect to work during their retirement years. Of the 4,626 people surveyed, 1,876 said they are either already working past traditional retirement age or anticipate doing so once they reach it. At first glance, the headline reads like a shift in lifestyle preferences. The underlying responses show something more complicated: that 40% comprises two very different groups, divided by whether they want to work or feel they have to.

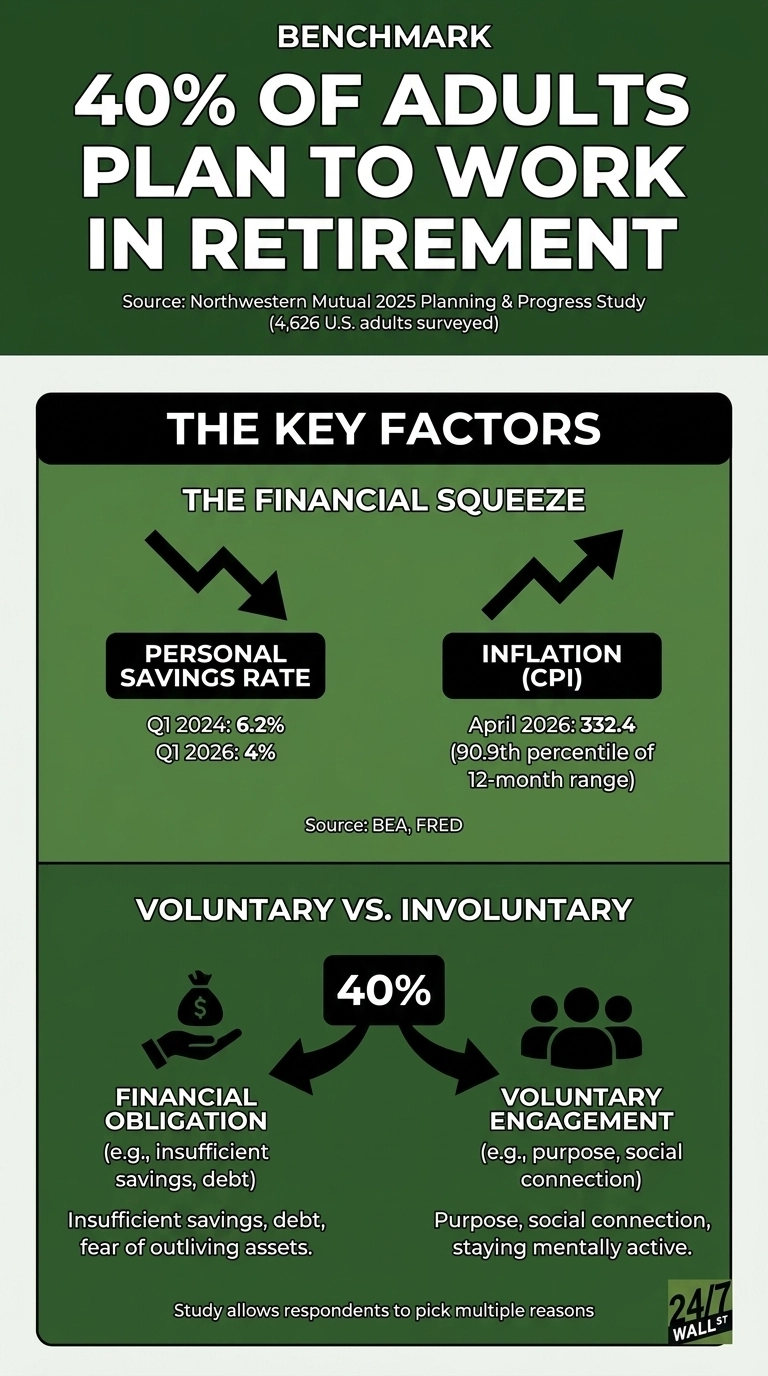

The split between voluntary and involuntary participation matters. Among the 1,876 who are working or planning to work in retirement, the survey captures both sides of the motivation curve. Some respondents point to purpose, social connection, or staying mentally active. Others cite financial pressure, including insufficient savings, debt, or the fear of outliving their assets. Northwestern Mutual allows respondents to select multiple reasons, which is why a single statistic can describe both the consultant who keeps a few clients for enjoyment and the retail worker who cannot afford to stop.

The economic backdrop pushing the “have to” group

The personal savings rate has been sliding at the exact moment households need it to rise. BEA data shows it falling from 6.2% in the first quarter of 2024 to 4% in the first quarter of 2026, even as per‑capita disposable income climbed from $63,638 to $68,617. Wages have been rising too, with average hourly earnings reaching $37.41 in April 2026, up from $34.47 in January 2024, yet consumption has grown faster than wages. Total personal saving dropped from $1,330.7 billion in early 2024 to $942.3 billion in early 2026, the lowest level in the BEA’s nine‑quarter window. Anyone wanting to explore this further can look at personal saving trends or household consumption patterns.

Inflation is doing the rest of the work. The Consumer Price Index stands at 332.4 as of April 2026, near the top of its 12-month range. Core PCE, the Federal Reserve’s preferred measure, has risen month after month for a full year, reaching 129.28 in March 2026. Persistent price pressure on fixed budgets is the condition that turns “I might work a little in retirement” into “I need the paycheck.” Readers who want to understand this dynamic can explore inflation’s impact on retirees.

Consumer sentiment reflects the strain with even greater clarity, as the University of Michigan index stands at 48.2 as of May 2026, a level that sits deep in pessimistic territory and well within the lower quartile of historical readings. The twelve‑month average is 55.6, with a percentile rank of 27.3, but the most recent reading captures the mood. Americans deciding whether to keep working are doing so against a backdrop in which confidence in the broader economy has slipped below the threshold typically associated with stability.

The Gen X squeeze

The Gen X numbers show the sharpest concentration of concern about retirement preparedness in the Northwestern Mutual study. Among the 3,796 non‑retirees surveyed, the anxiety is most pronounced in the cohort closest to the finish line. Gen Xers, now in their mid‑forties to early sixties, are the first generation expected to fund retirement primarily through 401(k)s and personal savings rather than the pensions that supported many of their parents. The study’s working‑age non‑retirees, a group of 3,562 respondents, reported starting ages and anticipated retirement ages that reveal how many began saving late and now face a shortened runway.

There is a generational shift inside the data as well. Among the 3,659 respondents who said their vision of retirement differs from their parents’, many expect to do more, not less, in their later years. They describe a retirement that includes travel, hobbies, time with family, and, in many cases, continued work framed as an active choice. That framing helps explain why the 40% figure is genuinely mixed. Some respondents are choosing engagement. Others are absorbing the consequences of a decade of declining household savings rates and rising costs.

What the labor market allows

The job market is currently cooperating with both groups. Unemployment is 4.3% as of April 2026, and initial jobless claims sat at 200K for the week ending May 2, 2026, near the lower end of the historical range. The Federal Reserve has cut its target rate to 3.75%, down from 4.5% a year earlier, which lowers yields on the safe savings vehicles retirees rely on but keeps borrowing costs manageable for households still working.

The honest read of the 40% figure is that it refers to two populations sharing a single statistic. One group is redefining retirement on its own terms. The other is responding to a savings rate that has been cut by roughly a third in two years, inflation in the 90th percentile, and a Social Security system that paid out $1.63 trillion in Q1 2026 but covers a shrinking share of pre-retirement income for most earners. It leaves a single conclusion on the table: the meaning of retirement now depends entirely on which side of that divide you land.

Contact [email protected] for any questions or corrections.