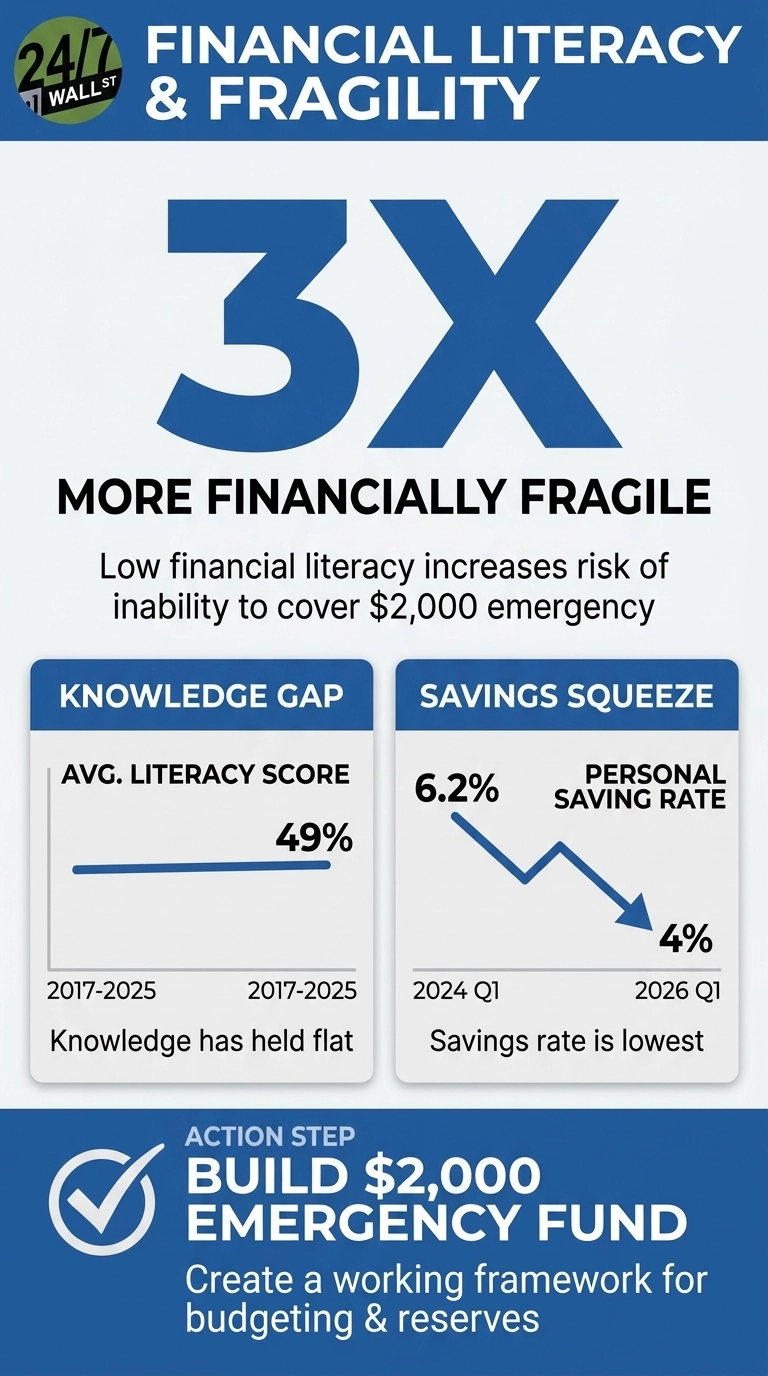

The TIAA Institute-GFLEC Personal Finance Index has tracked how much Americans actually know about money for nearly a decade, and the 2025 wave delivers a finding that reads less like a survey result and more like a structural diagnosis. Adults with very low financial literacy, defined as answering 25% or fewer of the index questions correctly, are three times more likely to be financially fragile than those answering 75% or more correctly.

The reality is that financial fragility has a specific definition, and it’s something everyone should know: it’s the inability to come up with $2,000 for an unexpected expense within a month. The framing matters because it converts knowledge into solvency and treats the gap between knowing and not knowing as a balance-sheet event rather than an academic one.

The Knowledge Line Has Not Moved

Since the index launched in 2017, U.S. adults have consistently answered roughly 49% of the P-Fin Index questions correctly, with no meaningful improvement from 2017 through 2025. Over that same period, the average household has been asked to absorb a pandemic, a refinancing boom and bust, the return of inflation, the highest federal funds rate in a generation, and the partial reversal of that cycle. Knowledge has held flat while the terrain has not, and the cost of that gap is evident in the macro data underlying the survey.

Personal savings illustrate the squeeze, arguably in the most notable of ways. While income has climbed to $68,617, those extra dollars are going out the door instead of into a safety net. The 2025 P-Fin Index shows that for households without a budgeting framework, a raise is almost always absorbed by increased spending. This lack of literacy is a direct barrier to financial stability, as adults with very low levels of literacy are 3x more likely to be financially fragile and 5x more likely to lack emergency reserves. Without these fundamentals, earners remain stuck below the critical $2,000 emergency bar, regardless of how much their paychecks grow.

The Gaps Show Up By Group

The 2025 P-Fin Index makes it clear that knowing how money works is the best predictor of whether you’ll actually have any. The data shows a brutal divide in financial well-being:

- Debt Traps: Adults with very low literacy are 2x as likely to be debt-constrained.

- Fragile Foundations: Those at the bottom are 3x more likely to be financially fragile, meaning they couldn’t scrape together $2,000 for an emergency.

- Zero Buffer: They are 5x more likely to lack even one month of emergency savings.

For Gen Z, this isn’t just a trend; it’s a daily reality. A massive 62% of Gen Z don’t have—or aren’t sure they have—one month of nonretirement savings. On top of that, 41% admit they’re stuck below that $2,000 emergency bar. While average earnings have climbed to $37.41 an hour, those gains are being swallowed by higher prices and shrinking safety nets. Without a solid framework for budgeting and compound interest, a raise is just absorbed by spending rather than building a cushion.

Risk Comprehension Is The Weakest Link

Across the eight functional areas the index measures, comprehending risk is consistently the weakest. Only 36% of adults answer risk questions correctly. Risk is also the input that matters most when the environment shifts. The University of Michigan Consumer Sentiment Index sat at 53.3 in March 2026, in the lower quartile of its 12-month range and within the band the survey calls “pessimistic”. CPI rose 3.7% from May 2025 to April 2026, and the federal funds rate has stepped down from 4.5% to 3.75% over the past year. Reading those three indicators together requires the exact functional area where the largest share of adults score lowest.

What The Data Documents

Initial jobless claims came in at 211,000 for the week ending May 9, 2026, and the unemployment rate sat at 4.3% in April 2026. Both readings fall within the range that the Federal Reserve considers healthy. The TIAA-GFLEC finding lands in that context, and even with a functioning labor market and rising nominal wages, a 4% personal savings rate and a tripled fragility ratio at the bottom of the literacy distribution describe the same population from two directions. The 2025 study treats financial knowledge as a precondition for absorbing ordinary shocks, and the macro data on savings, sentiment, and prices are consistent with what happens when that precondition is missing for roughly half the adult population.

Contact [email protected] for any questions or corrections.