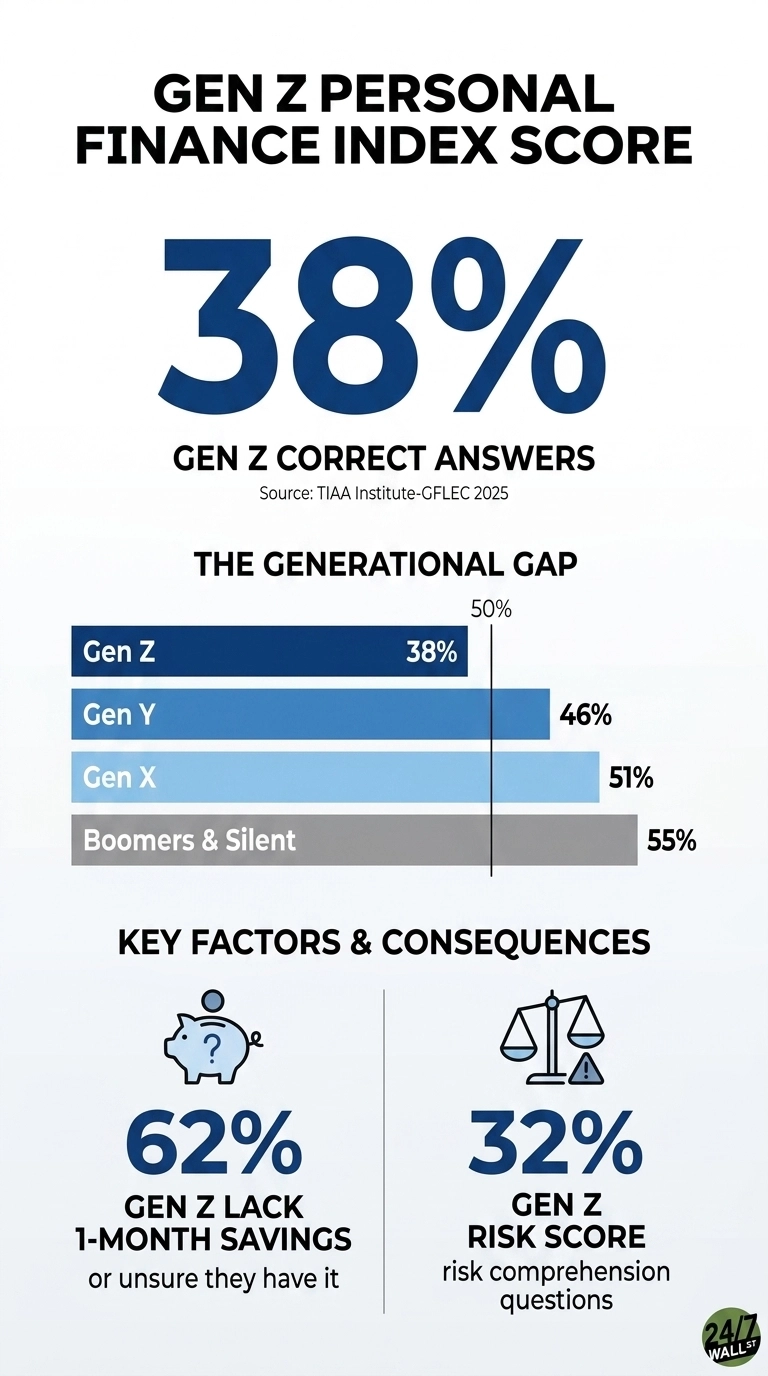

The 2025 P-Fin Index shows that Gen Z is entering the most complex economy in decades with the weakest set of tools. Averaging just 38% on the survey, this generation scored significantly lower than every older age group, reflecting a massive gap in functional knowledge. While the 4% savings rate and a shifting job market create enough pressure on their own, the real danger lies in what that 38% represents for young adults already feeling the squeeze.

This isn’t just about missing a few questions, it’s about the direct link between low literacy and financial disaster. Gen Z’s functional knowledge is substantially lower across all categories than that of older generations, particularly in insurance. When you realize that those with the lowest literacy are 3x as likely to be financially fragile and 5x as likely to lack emergency savings, it becomes clear that, for Gen Z, a 38% score is a warning light for their entire financial future.

The Generational Gap

The P-Fin Index reveals a massive generational divide that only widens with age. While Gen Y scored 46% and Gen X reached 51%, both Baby Boomers and the Silent Generation led the pack at 55%. This leaves a staggering 17-point gap between Gen Z and the oldest cohorts. Even more alarming is the bottom-heavy distribution for young adults: 37% of Gen Z fell into the “very low” literacy band, answering 7 or fewer questions, compared to just 10% of the Silent Generation. Essentially, more than a third of the youngest adults are operating without a basic functional understanding of their own finances.

What 38% Looks Like in Real Life

The P-Fin Index is more than a scorecard, it’s a direct predictor of your bank balance. The stats are brutal for those with very low literacy: they are 2x as likely to be debt-constrained, 3x more likely to be financially fragile, and 5x more likely to lack any emergency savings. For Gen Z, this isn’t just a trend, it’s a crisis. A staggering 62% of Gen Z don’t have, or aren’t sure they have, even one month of nonretirement savings. On top of that, 41% admit they couldn’t scrape together $2,000 for an emergency.

The cost of that fragility is hitting hard right now. While average earnings have climbed, those gains are being swallowed by higher prices and shrinking safety nets. In an era where the margin for error is getting thinner, a lack of financial fluency is the quickest path to a debt trap. Wage growth doesn’t matter if you don’t have the literacy to protect it from being eroded by a volatile market.

Nine Years, No Progress

U.S. adults overall have answered 49% of P-Fin questions correctly every year since 2017. Nine cohorts of high school and college graduates have passed through during that window, and the national average has not moved. The cost of getting things wrong has climbed during that same period. The federal funds rate sits at 3.75% as of May 14, 2026, which keeps credit card APRs and variable student loan rates near multi-year highs. Carrying a balance is more expensive than it was when this survey began.

The Weakest Link Is Risk

The index breaks questions into functional areas, including borrowing, saving, investing, insuring, and comprehending risk. Risk comprehension was answered correctly only 36% of the time across all respondents, and Gen Z scored 32% in that category. Risk understanding cuts across nearly every financial decision a young adult makes: choosing a health plan, deciding how much auto coverage to carry, evaluating a 401(k) fund menu, or sizing an emergency fund against a job market where the unemployment rate has drifted from 3.7% in January 2024 to 4.3% in April 2026. A gap in this category does not remain confined to a single decision.

What the Data Says, and What It Does Not

The P-Fin Index documents a measurable knowledge gap and its correlation with financial fragility. It does not show that closing the gap would erase the fragility, because some of what young adults face is structural: housing costs, student debt, and an unemployment rate that has been climbing. Consumer sentiment reflects the mood. The University of Michigan index reads 53.3 as of March 2026, which is historically in the lower quartile. The figures above show the starting position of young adults.

Contact [email protected] for any questions or corrections.