From Ballmer’s Shadow to a Cloud-and-AI Empire

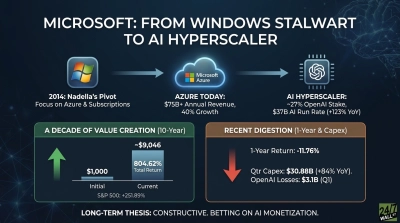

When Satya Nadella took over as CEO on February 4, 2014, Microsoft was still viewed as a Windows-and-Office licensing dinosaur. Microsoft (NASDAQ:MSFT | MSFT Price Prediction) traded near $30.03 on a split-adjusted basis that day. Today, it anchors the artificial intelligence (AI) buildout.

Nadella pivoted the culture, bet the balance sheet on Azure, moved Office to a Microsoft 365 subscription, and bought LinkedIn, GitHub, and Activision Blizzard. The OpenAI partnership, seeded with $1 billion in 2019, was restructured to a roughly 27% stake valued near $135 billion, with OpenAI committing to an incremental $250 billion in Azure services. Azure now runs at over a $75 billion annualized pace, and the AI business alone is at a $37 billion run rate, up 123% year over year.

What a $10,000 Stake Became

Using split-adjusted prices, here is how the math shakes out across standard horizons versus the S&P 500.

Since Nadella’s First Day

- Initial Investment: $10,000 (roughly 333 shares at $30.03)

- MSFT Total Return: 1,182.42%

- Current value: $128,242

- S&P 500 (same period): 330.44%

| Microsoft | S&P 500 | |

| 1-Year Return | −22.59% | 20.63% |

| 5-Year Return | 44.39% | 73.34% |

| 10-Year Return | 718.59% | 251.22% |

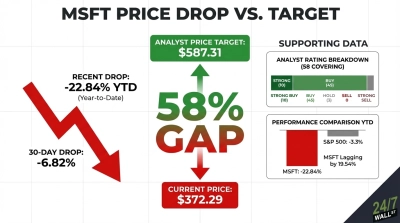

A $10,000 stake placed on Nadella’s first day is now worth many multiples of the original, before dividends. But the recent picture is ugly. Microsoft has slid from a 52-week high of $555.45 to $385.10, dragged by fears that capital expenditures of $30.88 billion (+84% year over year) will crimp free cash flow before AI revenue catches up. The five-year window even trails the S&P 500.

Grading Nadella, and the Succession Question

We have to give Nadella an A+. He inherited a roughly $300 billion company and built a $2.86 trillion one while lifting the quarterly dividend from $0.28 to $0.91. There is no confirmed news of any departure, but given his dual chair-and-CEO role, succession chatter is inevitable. A handoff to a proven operator like Scott Guthrie or Kevin Scott would likely reassure the market; a surprise external hire might not.

The Bull and Bear Case From Here

The bull case rests on the AI capex cycle producing durable Azure margin. Analysts are overwhelmingly bullish, and their mean price target is all the way up at $559.86, on a forward P/E near 21. The bear case builds if capital spending keeps climbing while Azure growth slips below 30%, which would signal that AI return on investment is stretching further out. Because Microsoft’s cloud business is growing fast and it has a massive backlog of guaranteed future revenue, the stock looks attractive at its current price.

Contact [email protected] for any questions or corrections.