PepsiCo, Inc. (NASDAQ: PEP | PEP Price Prediction) stands as a globally acclaimed titan in the beverage and snack industry. The conglomerate produces, markets, and distributes a vast array of food and drink items worldwide, boasting iconic brands such as Pepsi, Gatorade, Mountain Dew, Doritos, and Lay’s in its portfolio, which spans more than 200 countries. Positioned as a heavyweight contender in the non-alcoholic beverage and snack food arenas, PepsiCo competes with giants like The Coca-Cola Company (NYSE: KO) and Mondelez International Inc (NASDAQ: MDLZ). Together with its principal adversaries, PepsiCo commands a significant share of a global industry valued in excess of $550 billion. However, the growth rate has become slower considerably over the last decade, attributed to evolving consumer tastes and intensified competition from big and small players in the industry. Despite its impressive array of traditional food and beverage labels, PepsiCo confronts ongoing obstacles stemming from contemporary health trends and tightening household budgets. This challenges its ability to replicate its historic successes.

1. Valuation looks expensive

Investors need to evaluate if it is justified that a company has a higher P/E than the industry average

Despite a downtrend in stock prices, PepsiCo’s valuation appears steep when measured against conventional benchmarks. The firm’s Price-to-Earnings (P/E) ratio is pegged at 25.55, slightly below the S&P 500’s mean P/E of 27.3 but surpassing the industry norm of 22.09. Furthermore, a Price-to-Book (P/B) ratio of 12.46 suggests a considerable premium compared to both the market at large and its direct rivals. Given its modest earnings growth, these elevated valuation multiples seem hard to justify.

2. Declining cash flow

Declining cash flow can lead to a lower stock price.

A concerning indicator for PepsiCo is its dwindling net cash balance, as detailed in its cash flow statements, which has seen a decline from $5.3 billion to $3.1 billion over recent years. This trend hints at potential challenges in generating adequate cash to sustain operations and finance future expansions. Moreover, a year-over-year contraction of 29% in cash flow from operations further accentuates worries regarding its cash generation capabilities.

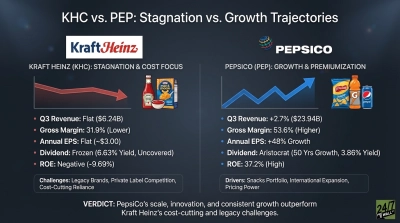

3. Face Intense Competition

Coke vs. Pepsi

PepsiCo operates in an exceedingly competitive beverage and snack market. Its main competitors, Coca-Cola and Mondelez, enjoy substantial scale and brand recognition. However, the market is also teeming with smaller entities that are gradually eroding market share across various segments. For example, PepsiCo’s staple cola and Gatorade offerings continue to enjoy consumer loyalty, yet flavored seltzer brands like La Croix have emerged as formidable competitors amid changing preferences. The snack section, too, offers endless alternatives, ranging from Frito-Lay’s Doritos to Annie’s organic bunny crackers, all vying for consumer attention. Today’s grocery aisles present shoppers with hundreds of alternative beverage and snack options, forcing PepsiCo to continuously defend its position in a market brimming with both established and emerging competitors. Misjudged pricing strategies or delays in adapting to the latest health trends could give competitors a window to challenge PepsiCo’s market leadership and erode its share. This relentless competition is likely to place ongoing pressure on financial outcomes.

4. Weak Organic Revenue Growth

Lay’s has several types of snacks contributing to revenue.

PepsiCo has reported a mere 5.9% increase in organic revenue over the past year, trailing the beverage subsector’s overall growth rate of 9.1%. The company’s flagship beverage division is under duress as consumer preferences shift away from traditional sugary sodas, while its snack labels struggle to appeal to an increasingly health-conscious demographic. This sluggish top-line growth poses challenges to margin improvement and puts long-term profitability targets at risk.

5. Inflation Eroding Profit Margins

When prices of raw materials goes up, it raises the cost of doing business. If this increased cost cannot be passed onto customers, the profit margin diminishes.

Like many in the consumer staples sector, PepsiCo is dealing with inflationary pressures throughout its supply chain and distribution networks. Costs for essential inputs such as aluminum, corn, oils, and transportation have surged. Despite efforts to mitigate these cost increases through strategic pricing adjustments, gross margins have declined by 40 basis points over the last year. Persistent inflation in inputs and logistics costs could significantly undermine PepsiCo’s profitability in the future.

6. Lagging Earnings Growth

Investors might need to wake up and take a closer look at the key drivers affecting PepsiCo’s financials.

PepsiCo’s earnings growth over the last 12 months was a modest 2.49%, which contrasts with the beverage subsector’s average earnings growth rate of 340.22% for the same period. With competitors achieving considerably higher profit growth, it becomes increasingly challenging to justify PepsiCo’s premium valuation metrics.

7. Weakening Financial Health

Pepsico might have a well-recognized brand but the company cannot rest on its laurels.

Examining PepsiCo’s balance sheet reveals a declining trend in financial health. The current ratio has decreased from 1.01 to 0.85 over the past three years, signaling potential short-term liquidity challenges. Moreover, total debt has escalated to over $47 billion, with cash reserves diminishing by 35% since the previous year. In an environment of weakening macroeconomic conditions, companies with significant leverage and liquidity issues like PepsiCo are likely to face greater difficulties compared to their less indebted counterparts.

In conclusion, while PepsiCo operates a robust business underpinned by globally renowned brands, it is confronted with numerous challenges, including high valuation, market saturation, fierce competition, input cost inflation, and a weakening balance sheet. Given these growing headwinds, investors might consider looking beyond PepsiCo stock at its current valuation. They could instead search for alternative investment opportunities with stronger growth prospects in a volatile economic landscape. Traders and investors should conduct their own analysis and consult a financial advisor as needed. This overview is not intended as financial advice.

About the author: Amit Nar can be followed on X @alphaintelligence and on discord.

Contact [email protected] for any questions or corrections.