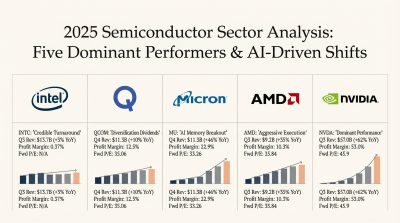

Headlines this week are obsessed with Intel Corporation (NASDAQ:INTC | INTC Price Prediction), which has ridden the agentic AI narrative and a parade of marquee partners to a 426.95% one-year run that has the chat rooms convinced the turnaround is in the bag.

But here’s what you should actually be watching.

The Intel Trade Has Already Happened

Intel is the textbook crowded trade. The stock is up 192.47% year to date, then dropped 13.61% in the past month as the June correction yanked the rug from under the most speculative chip names. Reddit sentiment scores collapsed from 55 to 78 in mid-May down to 12 to 39 by early June, with capitulation posts like “INTC 32k gains, I am out!” lighting up r/wallstreetbets. That is what a hype cycle unwinding looks like in real time.

The fundamentals do not support the rerating. Intel posted a GAAP net loss of $3.73 billion in Q1 FY2026, driven by a $4.07 billion restructuring charge tied to a Mobileye goodwill impairment. Free cash flow ran to negative $3.87 billion. Intel Foundry continues to hemorrhage cash, with operating losses of $2.51 billion in Q4 2025 alone. Trailing EPS sits at negative $0.60, return on equity is negative 2.91%, and the forward P/E carries a stomach-churning 123x. CEO Lip-Bu Tan himself called this a “deliberate reset,” which is corporate-speak for “this will take years.”

The Smart Money Pivot: Microsoft

A cleaner expression of the same AI thesis sits with Microsoft (NASDAQ:MSFT), trading at $403.41 after a 16.21% year-to-date pullback that has reset expectations without breaking the thesis. Three reasons it stands out for long-term investors to research.

One: monopoly-grade economics. Microsoft runs a 46.3% operating margin and a 34% return on equity, and printed $31.78 billion in net income in a single quarter. Intel cannot generate consistent positive net income at all. That is the difference between a toll booth and a lottery ticket.

Two: contracted future revenue. Commercial remaining performance obligations hit $627 billion, up 99% year over year, layered on top of OpenAI’s $250 billion incremental Azure commitment. That is multi-year visibility no chip foundry can match.

Three: AI exposure without the chip-cycle whiplash. Microsoft’s AI business cleared a $37 billion annual revenue run rate, up 123% year over year, with Azure growing 40%. No foundry losses, no 15% workforce cut, no U.S. government equity overhang. Satya Nadella said it plainly on the call: “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.”

Prediction markets agree on the floor. Polymarket traders assign a 92.5% probability Microsoft holds above $370 this week and a 63.5% probability of a $390 close into month-end. Analysts carry an average target of $560.95 with 52 Buy or Strong Buy ratings against zero Sell calls.

The Action

Look past Intel’s headline. Put Microsoft on your research short list, study the four consecutive earnings beats, and decide whether the toll booth fits your retirement plan.

Contact [email protected] for any questions or corrections.