Artificial intelligence has already reshaped the stock market. Semiconductor stocks have rallied, utilities are suddenly growth plays again, and hyperscalers are spending hundreds of billions of dollars building data centers across the U.S.

At the same time, President Donald Trump has pushed for more domestic manufacturing, energy production, and AI infrastructure investment as part of a broader effort to keep the U.S. ahead in the global technology race. But what if AI’s next phase doesn’t just create new companies? What if it creates an entirely new asset class?

That’s the argument BlackRock (NYSE:BLK | BLK Price Prediction) CEO Larry Fink made at the Milken Institute conference in Beverly Hills, speaking alongside Brookfield CEO Bruce Flatt. Fink warned that AI is already creating shortages across four critical markets: compute power, chips, memory, and electricity, as companies race to build ever-larger AI systems. He also pushed back directly on bubble fears, stating flatly that he does not see an AI bubble given that demand continues to outstrip supply.

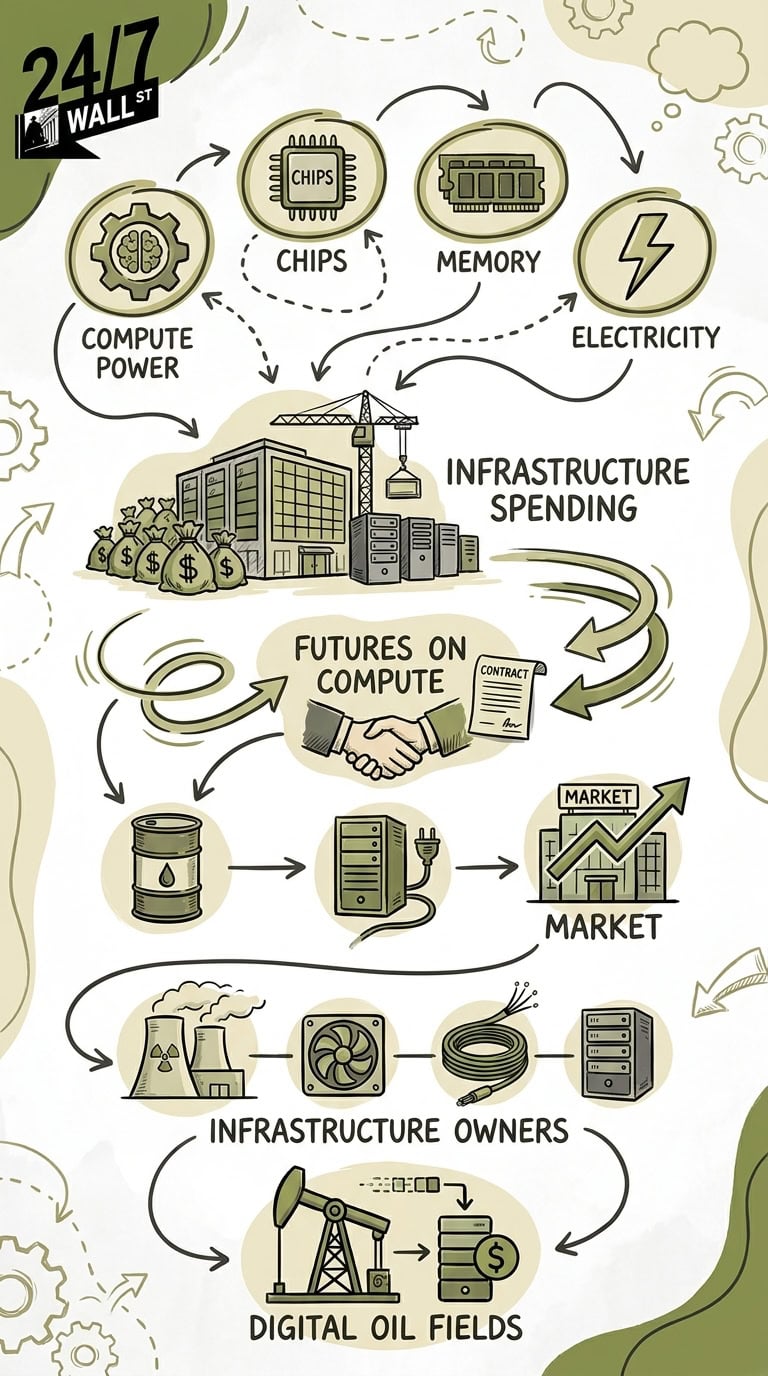

Those shortages are driving a wave of U.S. infrastructure spending tied to semiconductor manufacturing, power generation, and domestic data-center construction. Whenever essential economic resources run short, Wall Street finds a way to financialize them. Oil, natural gas, and electricity all evolved into massive futures markets. Fink believes AI infrastructure could follow the same path, potentially creating a trillion-dollar asset class centered on “futures on compute,” contracts tied to future access to AI computing capacity.

AI Is Turning Compute Into a Commodity

Every AI model, whether it’s ChatGPT, Gemini, Claude, or enterprise AI software, runs on computing power supplied by high-end chips and massive data centers. Those systems require GPUs from NVIDIA (NASDAQ:NVDA) and Advanced Micro Devices (NASDAQ:AMD), server infrastructure from Dell Technologies (NYSE:DELL) and Super Micro Computer (NASDAQ:SMCI), cloud capacity from Amazon (NASDAQ:AMZN), Microsoft (NASDAQ:MSFT), and Alphabet (NASDAQ:GOOG), and enormous amounts of electricity. AI doesn’t function without that entire physical stack behind it.

Goldman Sachs estimates global AI-related infrastructure spending could approach $1 trillion over the next several years. Microsoft, Amazon, Alphabet, and Meta Platforms (NASDAQ:META) are now projected to spend approximately $725 billion in combined capital expenditures in 2026 alone, up roughly 77% from the prior year’s record $410 billion, with much of that tied directly to AI infrastructure. Data center construction has roughly tripled since ChatGPT’s launch, and demand is still outrunning supply.

As demand for compute rises, pricing power rises with it. Instead of simply renting cloud capacity, companies may someday buy contracts guaranteeing future access to AI compute resources. Those contracts could take the form of GPU-hours, AI inference capacity, data center power allocations, or reserved cloud processing capacity. The analogy Fink reaches for is oil futures, where airlines lock in fuel prices months ahead of time. Only instead of barrels of crude, companies would hedge the future cost of AI processing power.

Why Wall Street Would Love Compute Futures

Financial markets thrive on scarcity and predictability. AI compute increasingly has both. NVIDIA’s Blackwell AI chips were effectively sold out through mid-2026, with major cloud providers placing orders in blocks of 100,000 units. At NVIDIA’s GTC 2026 developer conference, CEO Jensen Huang disclosed that the company had secured roughly $1 trillion in combined orders for its Blackwell and next-generation Vera Rubin architectures, spanning deliveries through the end of 2027. Microsoft executives have similarly acknowledged that AI infrastructure shortages constrained some cloud growth.

Once scarcity appears, Wall Street builds financial products around it. Electricity futures already exist. So do carbon-credit markets, uranium funds, and bandwidth pricing contracts. Compute could become the next step because AI has transformed processing power into an economic input rather than just a technology expense. That shift could radically alter the investing landscape.

Here’s what current valuations tell us about the companies already positioned closest to this trend:

| Company | Forward P/E Ratio | AI/Data Center Exposure |

| NVIDIA | 25 | Dominates AI GPUs |

| Broadcom (NASDAQ:AVGO) | 23 | AI networking/custom chips |

| Vertiv Holdings (NYSE:VRT) | 40 | Data center cooling/power |

| Constellation Energy (NASDAQ:CEG) | 23 | Nuclear power for AI demand |

| Digital Realty Trust (NYSE:DLR) | 23 (FFO multiple) | Data center REIT |

The market is no longer valuing AI solely as a software story. Infrastructure owners are commanding premium valuations because investors increasingly view compute capacity as a strategic resource rather than a commodity cost center.

The Hidden AI Story Is Actually Energy

Most investors still think of AI as a semiconductor story. In practice, it may prove to be an energy story disguised as a technology revolution. Goldman Sachs’ updated research projects that U.S. data centers will account for 8.5% of total peak summer power demand by 2027, up from roughly 4% in 2025. That acceleration is far faster than earlier forecasts anticipated, which helps explain why utility stocks suddenly entered AI conversations.

Companies such as Constellation Energy, Vistra (NYSE:VST), and NextEra Energy (NYSE:NEE) have all benefited from investor interest in supplying future AI power demand. That’s because compute requires not just chips, but also cooling systems, fiber networks, advanced memory, and semiconductor manufacturing capacity working in concert. AI’s next phase may reward infrastructure owners just as much as software developers.

Key Takeaway

Fink’s “futures on compute” concept may sound abstract today, but the market already behaves as though compute has become a scarce commodity. NVIDIA’s order backlog, hyperscaler spending races, and the sudden investor obsession with data-center electricity all point in the same direction. Fink himself has been explicit: he sees no AI bubble, only a supply problem that Wall Street will eventually financialize.

The deeper question is whether computing power itself becomes a tradable financial asset. If it does, the companies controlling AI infrastructure, chips, power, cooling, networking, and data centers, may matter as much as the software running on top of them. Owning the “digital oil fields” could prove just as valuable as building the applications they support.

Editor’s note: This article updates NVIDIA’s forward P/E to approximately 25 (from 19), revises the combined hyperscaler capital expenditure figure to approximately $725 billion for 2026, updates the Goldman Sachs data-center power forecast to reflect the bank’s latest projection of 8.5% of U.S. peak summer electricity demand by 2027, and adds context on NVIDIA’s roughly $1 trillion Blackwell and Vera Rubin order backlog disclosed at GTC 2026, as well as the Milken Institute setting and Brookfield CEO Bruce Flatt’s appearance alongside Fink.

Contact [email protected] for any questions or corrections.