Retail

Reality Check in Bed Bath & Beyond: Valuation and Chart Adjustment Ahead

Published:

Bed Bath & Beyond Inc. (NASDAQ: BBBY) is finally getting the dose of reality that should have been seen in 2013. The company’s earnings growth picture and margin picture is under pressure, and frankly this is a story that should be looking more mature by now. Missing earnings estimates and lowering guidance will only echo that stance on Wall Street. Source: Thinkstock

Source: Thinkstock

Analysts have chimed in to the downside after the earnings report. The retailer was downgraded to Neutral and the price target was cut to $78 from $85 at Credit Suisse. Canaccord Genuity lowered its price target to $73 from $84 after the earnings report, while Oppenheimer lowered its target to $86. Citigroup dropped its target to $85.

Bed Bath & Beyond reported on Wednesday that its third-quarter earnings came in at $1.12 per share, while revenue was $2.86 billion. We had the consensus at $1.15 in earnings per share and revenue of about $2.88 billion.

Guidance is where things really went off the track. Fourth-quarter earnings guidance was $1.60 to $1.67 per share, down from a prior forecast of $1.70 to $1.77 per share and well under the consensus estimate of $1.79 per share.

Full-year guidance went down to $4.79 to $4.86 in earnings per share, from a prior range of $4.88 to $5.01 per share and short of the consensus estimate of $5.02 per share.

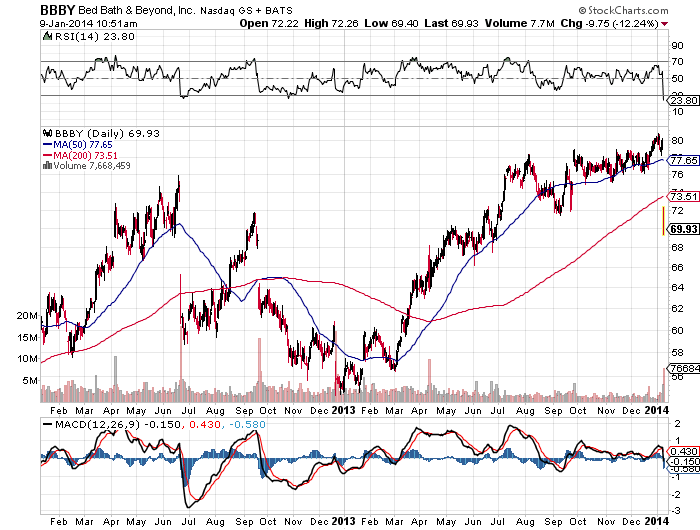

The stock’s chart is where this story becomes very complicated. This marks the fourth major gap down in two years, and the gap takes the stock back to under where the first pre-gap price was. Long-term investors who rode this growth wagon should be paying attention, because this is a chart pattern that is usually very hard to expect any snap-back rally from.

The stock needed to hold above $72, but the late-morning trading on Thursday shows the price down a sharp 12% at $69.80 on about six times normal trading volume of 8.3 million shares. The high for the day was $72.26, implying that the chart failure took place almost immediately after the open. Anything can happen, and many investors have made real money buying the big dips when it comes to Bed Bath & Beyond, but it now seems that investors may need to wait for another big dip before expecting serious gains.

Trading at 14.5 times expected earnings is not exactly an expensive earnings multiple. The problem is that Bed Bath & Beyond is becoming a regular disappointer when it comes to earnings. It cannot command a higher premium with a damaged credibility. This company also still somehow has not paid a dividend to its holders.

What we find even more interesting is that bed Bath & Beyond would have known about weak Black Friday and weaker sales for weeks now. Don’t say you were not warned if this one fails to snap back soon.

Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes. Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests. If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Thank you for reading! Have some feedback for us?

Contact the 24/7 Wall St. editorial team.