It is no secret that investors love dividends. With dividends generally expected to account for one-third to half of total returns over time, investors need to understand that not all dividends are created equal. Some companies can fund healthy dividends, with payout hikes announced for years in a row and years into the future. Other companies fund dividends through cash flows rather than just from earnings. Some companies rob their own treasury and will go to whatever means are necessary to maintain a high payout.

The big question is whether a company that has been in trouble will be forced to slash its dividend. In the case of Kraft Heinz Co. (NYSE: KHC | KHC Price Prediction), there is now a debate about whether the company can (or should) maintain its current payout.

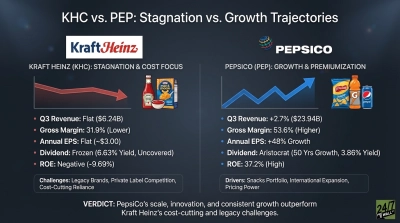

The current $1.60 per common share dividend paid out to Kraft Heinz shareholders generates a 5.47% dividend yield, based on a $29.25 share price. Where things get messy is that Kraft Heinz would seem to have ample dividend coverage based on the past earnings of $3.53 per share, but the Refinitiv estimates are $2.80 in earnings per share for 2019 and $2.55 per share in 2020.

Note that Kraft Heinz already cut its payout once before. The dividends were $0.625 per common share throughout half of 2017 and all through 2018. If Kraft Heinz decides to lower its dividend again, it could set up an entirely new round of frustration by shareholders.

Before Kraft Heinz feels like it is being picked on here, the issue to consider is that the company botched its operations over recent years since the 3G and Berkshire Hathaway transaction. This was more than a $90 stock back in 2017, and it is down over two-thirds from that peak even today. The problems here are too many to list, and there is a hope that the company is remedying some of its woes under new management. That said, there still likely will be a persistent belief that Kraft Heinz does not sell the food products that excite younger buyers, who are increasingly becoming more vocal and more important when it comes to overall food buying trends.

[nativounit]

Credit Suisse has an Underperform rating and a $27 price target for the shares. The firm’s Robert Moskow has recently lowered sales expectations, but the firm also said that a dividend cut appears to be imminent. His report said:

Debt rating agencies have said that they need to see evidence that Kraft Heinz has stabilized its EBITDA (now at $6.0B) and is on-track to reduce its leverage below 4.0x by mid-2021. However, we expect a step-down in EBITDA in 2020 of $200M just from divestitures and incentive compensation alone. If so, we do not see how the company can achieve the rating agencies’ targets unless it cuts its dividend. We think that management would announce this decision on its 4Q earnings call rather than wait until the release of its Enterprise Strategy in early 2020. According to Bloomberg on February 3 (function OVDV), the options expiring on March 6 imply that the 1Q20 dividend will be cut to $0.22 (down -45%). Short-sellers appear to believe that the bad news is already in the stock, with short interest down 11.7% to ~14.7M shares over the past three months (26% below its 12-month average). The options market is implying an 8% move on earnings day.

Not all firms expect a dividend cut from Kraft Heinz.

Independent research firm Argus raised its 2019 adjusted earnings estimate on February 4 to $2.80 per share from $2.66 per share, but the firm also reduced its 2020 EPS estimate to $2.55 from $2.65. The firm’s combined dividend-specific commentary in the latest report said:

If we needed to make another reduction to our earnings estimates, that would weaken our assessment of dividend stability and reduce the company’s financial flexibility to rejuvenate sales… We are keeping our 2020 dividend estimate of $1.60. Our dividend estimate for 2020 is approximately 63% of our earnings estimate for the year. We would like to see the payout rate decline as a result of rising earnings. Sixty percent isn’t particularly high, but we would like it to be lower so the company has more cash to reinvest in the business or reduce debt.

CFRA has a Hold rating and a $33 target price, and the firm had a bit more comfort that the company can maintain its current dividend payout based on its most recent earnings report.

Kraft Heinz should have been a defensive stock leader, based on its exposure to mass market food production. Yet, the company got in its own way and has not evolved with the newer trends that drive food demand. Its shares were as low as $25 last August, but the rally back up to $33 before year-end proved to be too much gain in the stock for too little gain in the fundamentals. Its shares have slid lower in 2020.

The consensus analyst target price from Refinitiv is $30.95, but shares traded closer to $29 on last look. Most analysts remain cautious here due to years of potential headwinds. Even after the drop that was seen over the prior two years, Kraft still has a market capitalization of nearly $36 billion.

[recirclink id= 643400]

[wallst_email_signup]

Contact [email protected] for any questions or corrections.