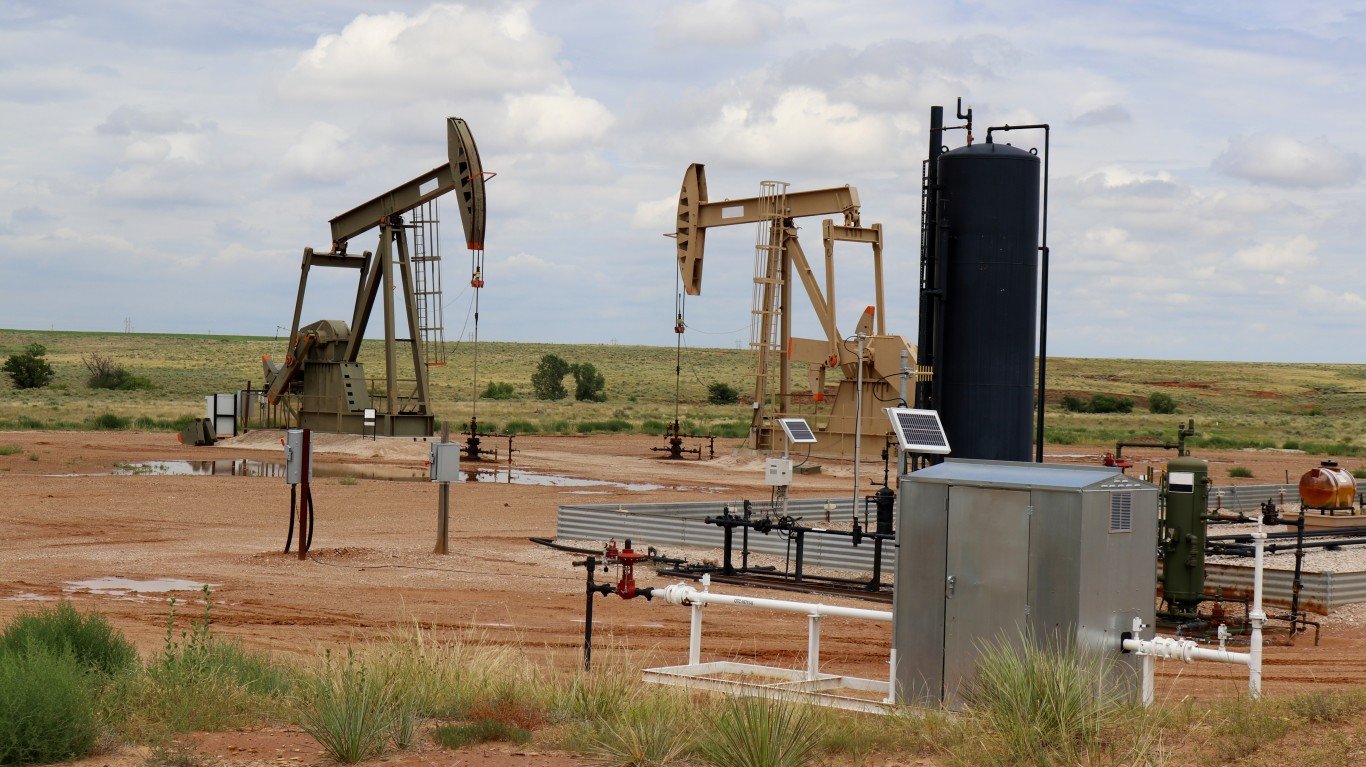

The price of West Texas Intermediate crude oil had risen by about 0.5% in the noon hour Wednesday to $39.99, remaining pretty solidly in a three-month range of around $37.50 to $42.50. Crude prices peaked at around $62 a barrel in early January, before the devastation of the COVID-19 pandemic became fully clear.

The Dallas Federal Reserve on Wednesday released its third-quarter report on the state of the oil market in the 11th Federal Reserve district. While business activity has picked up significantly, the index of business activity remains negative. From an index reading of −66.1 in the second quarter, the third-quarter index rose to −6.6, “suggesting that the pace of the contraction has significantly lessened,” according to the Dallas Fed’s analysts.

On average, survey respondents expect a WTI price of $43.27 a barrel by the end of the year.

The Fed analysts also asked several special questions related to the role of the Organization of the Petroleum Exporting Countries in determining future crude oil prices. The answers are enlightening.

[nativounit]

Nearly three-quarters of respondents (74%) believe OPEC will play a bigger role in setting the future price of oil and nearly two-thirds (66%) believe U.S. crude oil production has peaked. For the past dozen years or so, however, when OPEC has managed to drive the price higher, U.S. producers jump in when prices reach around $50 a barrel. The overall effect is to lower prices by a lot before they stabilize again in a narrow range of around $40 to $45 a barrel.

One commenter noted that the U.S. is in a period of transition away from fossil fuel: “Going forward, large investment pools of capital will not invest in petroleum. I have lived through several industry booms and busts, but this one is different.”

Another comment suggested that global oil demand will rise to pre-pandemic levels of “100-plus” million barrels a day by late next year and that oil prices could jump to more than $70 per barrel or more as demand outstrips supply: “Thus, the vicious boom/bust cycle in the oil industry will continue in 2022–24 as oil companies overinvest, while demand is being destroyed due to high oil prices ….”

In order for oil production to rise, most firms (73%) included in the Dallas Fed’s survey think the price for WTI has to rise into the $50 to $60 price range. More than half (54%) say that a price of $41 to $50 a barrel would increase completions on drilled but uncompleted wells. According to the U.S. Energy Information Administration, there were 7,665 such wells in the seven major U.S. onshore shale plays at the end of August, a month over month drop of 77.

The Dallas Fed reported that oil production improved quarter over quarter as well, rising from an index score of −62.6 to −15.4. The natural gas production index score rose 38 points sequentially to −10.1.

Capital spending for exploration and production companies also remains negative but rose by 49.7 index points to −16.4. Spending continues to decline, just not as much.

Oilfield services, perhaps the hardest hit of any sector of the energy business, also saw some improvement. The outlook remains negative but it did jump by 50 index points to −18.9 in the third quarter. Capital spending for services firms also improved, from −73.5 in the second quarter to −35.1 in the third quarter.

In the first six months of this year, Texas oil and gas companies laid off 61,000 employees, the Dallas Fed reported, representing about 26% of the pre-pandemic workforce in the state. That total does not include the 20,000 employees that oilfield services firm Schlumberger said it will cut later this year.

[recirclink id=768967][wallst_email_signup]

Contact [email protected] for any questions or corrections.