The world has changed in very short order as a result of the COVID-19 pandemic. The raging bull market of 11 years has died and the bear market drops of 30% and the economic pain recession have dealt a serious blow to the economy. Investors have historically moved into safe-haven assets in times of turmoil because of stable business models and steady earnings that allow them to pay dividends through hard times. The utilities sector is supposed to be about as safe as it gets. After all, everyone has to have electricity, heat or air-conditioning, and water to live in the 21st century.

Now there is a new question. What happens to earnings predictability for even the safest of companies when the world is turning upside down and when millions of customers’ jobs vaporize simultaneously? It is becoming nearly impossible to predict any long-term earnings, and it looks as though there is a serious risk that customers either will be unable to pay or will be very slow at paying their monthly bills.

Over the past decade, the safe income and revenue streams, predictable earnings and high dividends allowed the investing community to treat utilities as a modern version of those old certificates of deposit that banks would issue. Is that now at risk? The rapid onset of the current recessionary climate has been much faster than what has been seen, even compared to the financial crisis in 2008. The good news this time around is that many companies were financially healthy at the onset.

24/7 Wall St. has evaluated the utilities sector for years. It seems almost impossible and even feels treasonous to consider that utilities could potentially have problems with their dividends. While this is not a prediction that utility dividends are at risk, it is imperative to look at realistic earnings and revenue expectations for dividend coverage to see if these payouts are indeed safe. As it stands right now, the dividends should be safe. Assuming that the jobless claims cross 1 million in a week, what happens when those numbers of layoffs keep climbing sharply? Every one of those people losing a job has a need for the utilities to keep operating.

After searching through the top utilities in the S&P 500, we looked at the dividends paid per share and matched these up against earnings. Refinitiv was used for showing future earnings expectations, but it is growing impossible to trust what actual revenues and earnings ahead will really be, considering the deterioration in the business world and the pain that is happening at the population level.

[nativounit]

Note that a fresh report from Fitch Ratings showed how the coronavirus fallout will lower public power demand and lower its affordability:

US public power systems are expected to face limited immediate credit pressures related to the spread of the coronavirus, but an economic slowdown will weigh on longer-term performance, says Fitch Ratings. Significantly lower electric demand poses the most significant near-term risk for public power systems. While Fitch expects most systems to support revenue requirements and operating margins by raising retail rates, declining levels of employment and household income could strain affordability metrics over time and undermine rate-setting strategies, weakening credit quality.

While Fitch Ratings did not address future dividend payments, there is a warning that long-term business interruptions, pressure on median household income and the woes of the economy could help to weaken credit metrics and also trigger rating actions for utilities on the cusp of a lower rating category. The price erosion in the utility stocks has been massive already.

To show just how much destruction has been seen in the utilities sector as a whole, the Utilities Select Sector SPDR Fund (NYSEARCA: XLU) has seen its shares fall to $51.75, after peaking at $71.10 as recently as February 18. While a drop of 30% in the stock market is nowhere close to a normal event, the defensive utility sector would have normally been a go-to safe-haven trade for investors. Now utilities are basically letting customers know that their services will continue and some have joined the waves of other sectors where the companies are drawing down their credit lines to bolster their financial liquidity.

24/7 Wall St. evaluated the largest utilities that also have higher dividend yields for expected dividends yields, earnings per share (EPS), revenues and just how much the shares have dropped from their recent peaks. With the selling that has been seen, it is obvious that investors have used these as a source of funds and to lock in major gains over time. That said, the dividend issues need to be considered if the coronavirus recession is going to be a deep and lasting event.

[recirclink id=656783]

NextEra Energy Inc. (NYSE: NEE) is the only U.S. utility that has ever hit a $100 billion market cap. Its shares peaked at $283.35 but were last seen at $206.00. The $5.60 per share dividend generates a 2.7% yield and is against 2019 earnings of $8.37, as well as consensus estimates of $9.08 EPS in 2020 and $9.85 EPS in 2021. Revenue growth was last seen with consensus estimates of 3.7% for 2020 and 4.6% in 2021.

Dominion Energy Inc. (NYSE: D) has a $59 billion market cap, and the $3.76 dividend per share generates a yield above 5%. That said, its share price of $70.50 is now down from a peak of $90.89. With a $3.76 per share payout, its 2019 earnings were $4.24 per share and consensus estimates are $4.39 EPS in 2020 and $4.63 EPS in 2021. Revenues are forecast to rise 12% in 2020 and 3.2% in 2021. Dominion recently announced a $500 million equity shelf registration after showing it plans to have an at-the-money shelf if needed, with the use of proceeds being for the use of debt repayment and for funding capital expenditures.

Duke Energy Corp. (NYSE: DUK) was trading close to $74.00 with a 5% dividend yield. Its $3.78 per share dividend payout is against last year’s $5.05 EPS and estimates of $5.24 EPS in 2020 and $5.46 EPS in 2021. The consensus revenue growth is 4.6% for 2020 and 3.1% for 2021. Duke recently drew $2 billion on its credit facilities to cut its outstanding commercial paper (short-term debt) and for general corporate purposes. It also issued $400 million in new corporate debt this week.

Southern Co. (NYSE: SO) has a market cap of $53 billion. Its shares peaked at $71.10 but were last seen at $50.50 with a 4.8% yield. The $2.48 per share dividend is against 2019 earnings of $3.11 and consensus estimates of $3.18 EPS in 2020 and $3.31 EPS in 2021. Revenue growth was last seen with consensus estimates of 3.7% for 2020 and 2.4% in 2021.

American Electric Power Co. Inc. (NYSE: AEP) has a $38 billion market cap. Its shares peaked at $76.68 but were last seen at $77.10. The $2.80 per share dividend is against 2019 earnings of $4.24 and against consensus estimates of $4.38 EPS in 2020 and $4.67 EPS in 2021. Revenue growth consensus estimates were 7.8% for 2020 and 3.3% in 2021. AEP yields roughly 3.5%, and this company has traditionally been as big of a dividend defender as any company could ever hope to be.

Consolidated Edison Inc. (NYSE: ED) has a $26 billion market cap. Its shares peaked at $95.10 but were trading at $77.92. The $3.06 per share dividend is against 2019 earnings of $4.38 and consensus estimates of $4.44 EPS in 2020 and $4.62 EPS in 2021. Revenue growth consensus estimates were 4.6% for 2020 and 3.3% in 2021. Con-Ed’s dividend yield is roughly 3.8%. On March 13, it announced that it was suspending service shut off actions in New York City and Westchester.

Exelon Corp. (NASDAQ: EXC) has a market cap of $32 billion. Its shares peaked at $51.18 but were last seen at $32.87. The $1.53 per share dividend is against 2019 earnings of $3.22 and consensus estimates of $3.14 EPS in 2020 and $2.99 EPS in 2021. Revenue growth consensus estimates were −7.8% for 2020 and 0.30% in 2021. Exelon’s dividend yield is about 4.7%. Its ComEd unit also announced it was suspending disconnects, and Fitch recently affirmed its BBB+ ratings with a stable outlook.

Again, it feels like treason even to ponder if the major utilities in America would have dividend risk. Unfortunately, these new times have brought potential unthinkable outcomes with which a historic playbook is of little or no real help.

[recirclink id=656714]

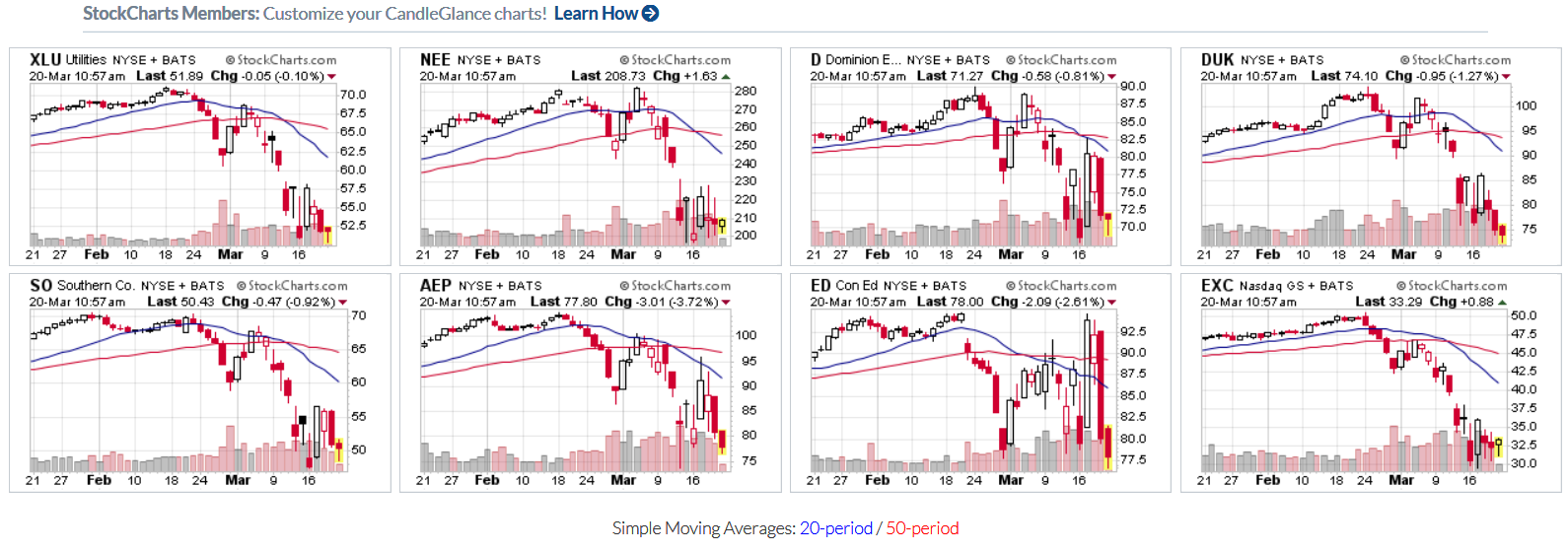

This chart montage from StockCharts.com shows the shareholder destruction since these peaked in February.

[wallst_email_signup]

Contact [email protected] for any questions or corrections.