If there’s one thing Americans love talking about, it’s retirement. How much do you need to save for retirement, how old do you have to be to retire, what to do when you retire, will the government steal from Social Security to pay for tax cuts for the rich, and how will the latest market event affect my retirement?

Hypocritically, for a nation absolutely obsessed with hard work and “earning” a living, we certainly think a lot about the time when we won’t have to work anymore and brag a whole lot about being able to retire “early”.

Naturally, the threat of living out our retirement years struggling to survive on Social Security even though we worked a full job our entire lives forces us to worry about our retirement savings from the first day we start working to the last minute we clock out. Unlike other developed countries that actually provide for the poor, needy, and elderly, America’s me-first attitude leaves millions of people worried sick about their future, unable to fully enjoy the present because the future is always looming. Even if you do everything correctly, the actions and decisions of others in your company or elected office could make it all meaningless.

For example, Larry Fink, the CEO of the largest asset management company in the world, Blackrock, and a person worth over $1 billion says that retirement at 65 years old is “a bit crazy”. Extreme right-wing personality Ben Shapiro also recently advocated for raising the retirement age to 67. When the people who own the companies you work at, eat at, and depend on, and the people who are desperate to retain political power, are both advocating for making you work until you die, you might begin to think there is a problem

You could work your entire life and follow the rules and still not be able to afford retirement. If you make it to retirement age and realize you don’t have enough saved up, tough luck. There are no systems to help you besides Social Security. If things continue down this track, we might be lucky to enjoy a few minutes of retirement before we die.

According to professional psychologists, social scientists, and development experts, your 30s are meant to be the time when you complete your self-discovery and begin to dive into your work career. Your brain has finished growing, you have finished your formal education, and should have spent a few years discovering the kind of person you are and how you want to spend your life.

Unfortunately, according to many in the United States, however, you should already have been working a full-time job for at least a couple of decades by then and have more money saved up by 35 than some people in the world see in their entire lives. How much do you need, exactly? And to answer your silent question: how far behind are you?

How Much Should You Have Saved For Retirement?

It is possible to enjoy your retirement.

As with all of life’s most complicated questions, the answer is: it depends. But there are some general benchmarks that you should be striving for if you want to have at least a fighting chance of surviving past retirement. Keep in mind, however, that all these benchmarks, goals, and guidelines are all set by industry insiders, financial institutions, and investment professionals. The most financially successful are the ones setting these goals for you. Make of that what you will.

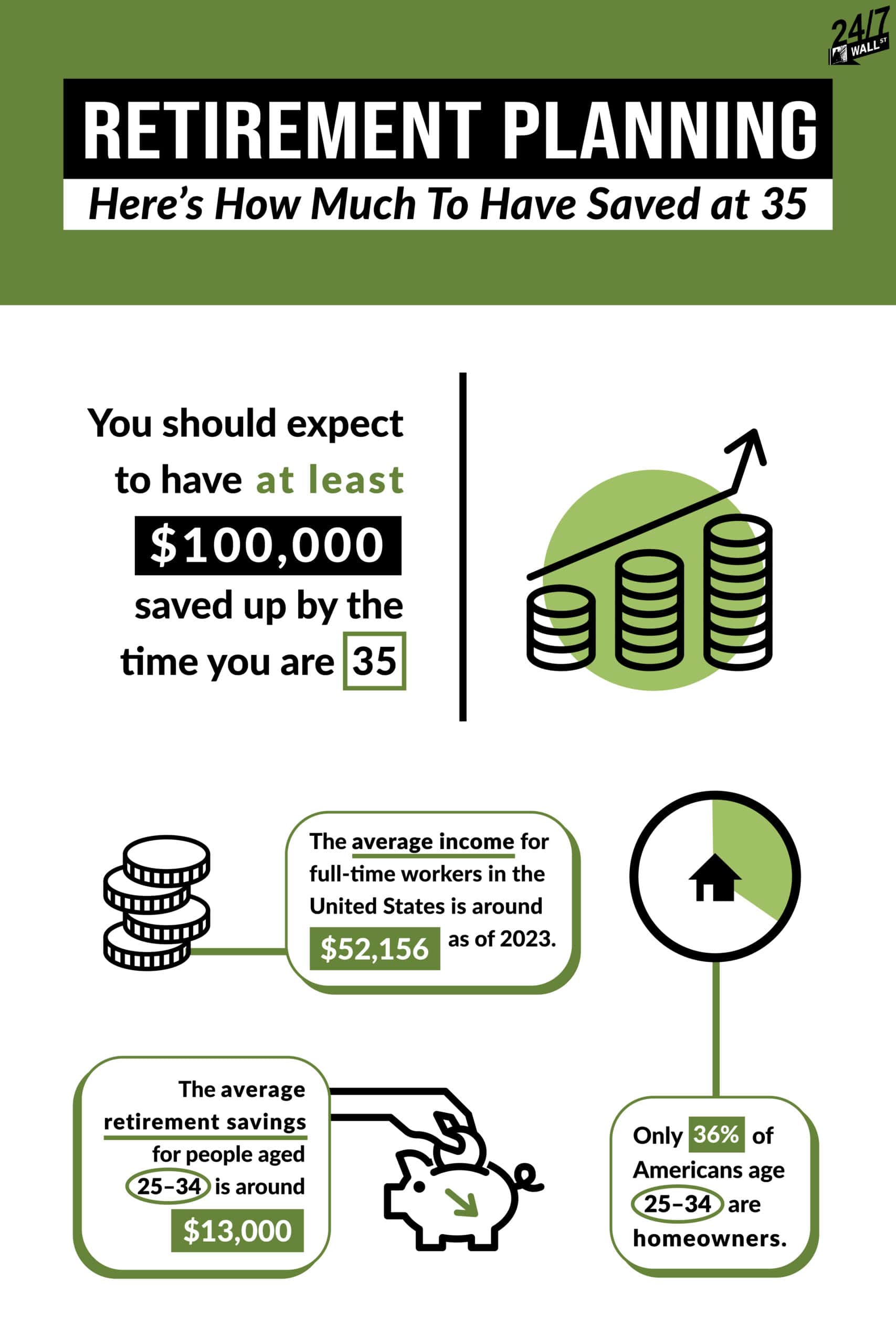

The first rule of thumb is that you should have at least double your annual income saved for retirement by the time you turn 35. The average income for full-time workers in the United States is around $52,156, as of 2023. That means you should expect to have at least $100,000 saved up by the time you have your 35th birthday.

Where do you stand compared to the average?

If your stomach just dropped while reading that and feel like you’re so far behind you might never catch up, you’re not alone. The average retirement savings for people aged 25–34 is around $13,000, and only 36% of them are homeowners. Naturally, the high earnings of the extremely wealthy skew these numbers higher.

During this age, most people are starting families, finally settling into their long-term careers, and actually starting to learn about retirement. Combine with this the fact that financial experts recommend having an emergency fund that can last for six months, and it’s no surprise that most people have nowhere near $100,000 saved up. This is just for the average American, too. Those who are first-generation migrants, have expensive diseases or surgeries, family members that they have to support, or other financial burdens might never have any retirement savings at all by the time they turn 65.

Another Way to Decide How Much To Save

A view of the American Dream.

A better way to calculate how much you need to have saved up for retirement is to predict how much you will need when you retire and reverse-engineer those numbers to your current age.

First, take a guess on how long you think you might live after age 65. Ten years? Twenty?

Second, guess how much you plan to spend every year during retirement. To make it easy, you can take your annual living expenses today and subtract the amount Social Security would be for an entire year.

Third, multiply the resulting amount left over by the number of years you hope you spend in retirement. That number is the amount you need to have saved up by the time you are 65.

Fourth, take that amount and plug it into an online financial calculator that can calculate the rate of growth with interest over the next thirty years. The more money saved now, the faster it will grow than the same amount saved near retirement, so simply dividing your retirement goal by the number of years results in unrealistic savings goals.

So, for example, the average annual expenses for a family of two in the United States was $76,468 in 2022. The maximum social security benefits for 2024 are $58,476 per year. So, if you plan to live for twenty years after retirement, you will need to save $359,840 for retirement. If you don’t plan on getting Social Security, or don’t qualify for it at all, you will need to save up over $1,500,000 all by yourself.

It might seem overwhelming, but this doesn’t include the power of compounding interest and the growing value of retirement accounts. A large portion of that amount can come from interest earned over the next thirty years if you choose an account wisely, like Robinhood’s IRA account with a contribution match.

Of course, remember that not everyone qualifies for the maximum Social Security payment, and some of your expenses will include income taxes. Yes, you will be taxed on the money you saved up.

Does all that money have to be in a specific retirement account? Not necessarily. While it might be a good idea to have that money set aside in a separate account like an IRA or investment account, as long as you keep track of your personal finances responsibly, your “retirement” account can be whatever you want.

All this being said, is this measure realistic anymore? Even if you manage to meet or exceed retirement expectations there is no guarantee that the government or the extremely wealthy won’t pull the rug out from under you as you approach retirement age. There are those who will remain determined to squeeze every last second of productivity out of your life until you die from exhaustion. The most reliable way to ensure you are prepared for retirement is to reduce your expenses as you age, create and participate in a community or a family that cares for its members, save as much as you can without sacrificing the joy of today, and advocate vigorously for change.

Contact [email protected] for any questions or corrections.