Refinance activity is driving much of the mortgage market right now. They noted:

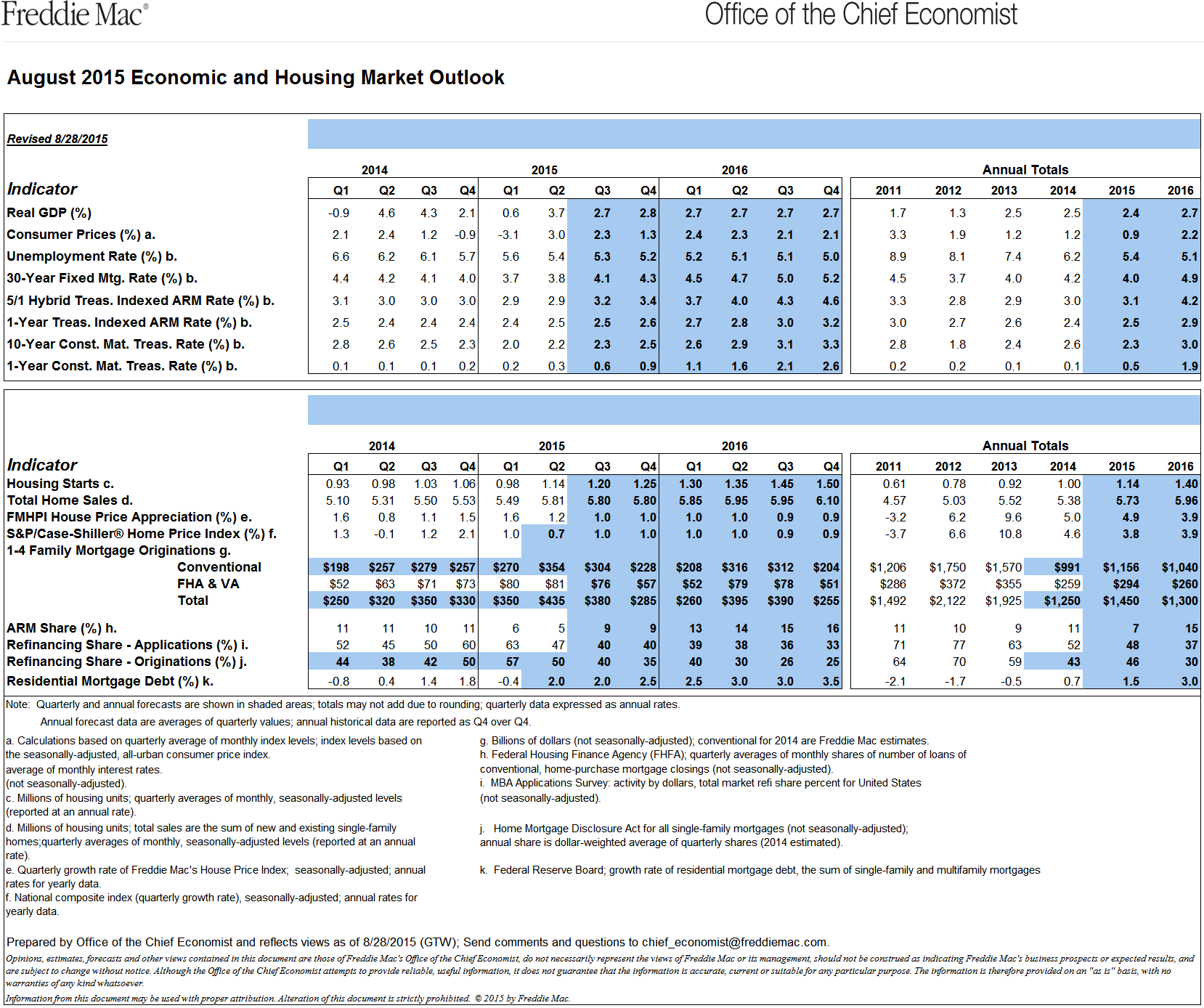

- Due to stronger-than-expected refinance activity and home sales, estimate of 2015 mortgage originations have been increased to $1.45 trillion and 2016 originations to $1.3 trillion.

- Increased projection of 2015 home sales to 5.73 million units, which would be the best year since 2007.

- Revised 2015 refinance share up to 46% of all single-family mortgage originations.

Here were some of the second quarter refinance highlights for 2015:

- Cash-out refinances increased from 27% of refinances in the first quarter of this year to 34 percent in the second quarter. A year ago, the cash-out share was 22 percent. During the housing boom, the cash-out share peaked at 89 percent in the third quarter of 2006.

- An increasing share of refinancing borrowers chose to shorten their loan terms. Of borrowers who paid off a 30-year fixed-rate loan in the second quarter, 40 percent chose a 15-or 20-year loan, compared to 39 percent in the first quarter.

Freddie Mac compared actual losses on low down payment loans to losses on 20% down payment loans over the 10-year period 2003-2013. This includes the housing crisis, as follows:

- 30-year fixed rate loans with 3% down payments were 17% riskier than 20% down payment loans over that period. They did note that it was “only” that much riskier.

- 7/1 ARMs were 155% riskier than 30-year fixed rate mortgages over the same period.

- 5/1 ARMs were 5-times as risky than 30-year fixed rate mortgages over the same period.

- On affordability, Freddie Mac said that there is a surprising amount of disagreement among the various measures of overvaluation. The same metro area may be tagged as overvalued by one metric and undervalued by another measure.

An image of a table has been provided from Freddie Mac, along with 2015 and 2015 outlooks in economic readings and on housing statistics:

Contact [email protected] for any questions or corrections.