Car prices rose sharply during the COVID-19 pandemic. A shortage of parts kept new car inventories very low. Many car models sold for well above the manufacturer’s suggested retail price. Manufacturers were upset by that because they believed it alienated customers. Dealers found it was a way to pad their margins. Prices rose so quickly that the median price of a new car was $40,000. Only one new car model costs below $20,000: the Mitsubishi Mirage. (These 15 cars hold on to their value the longest.)

[in-text-ad]

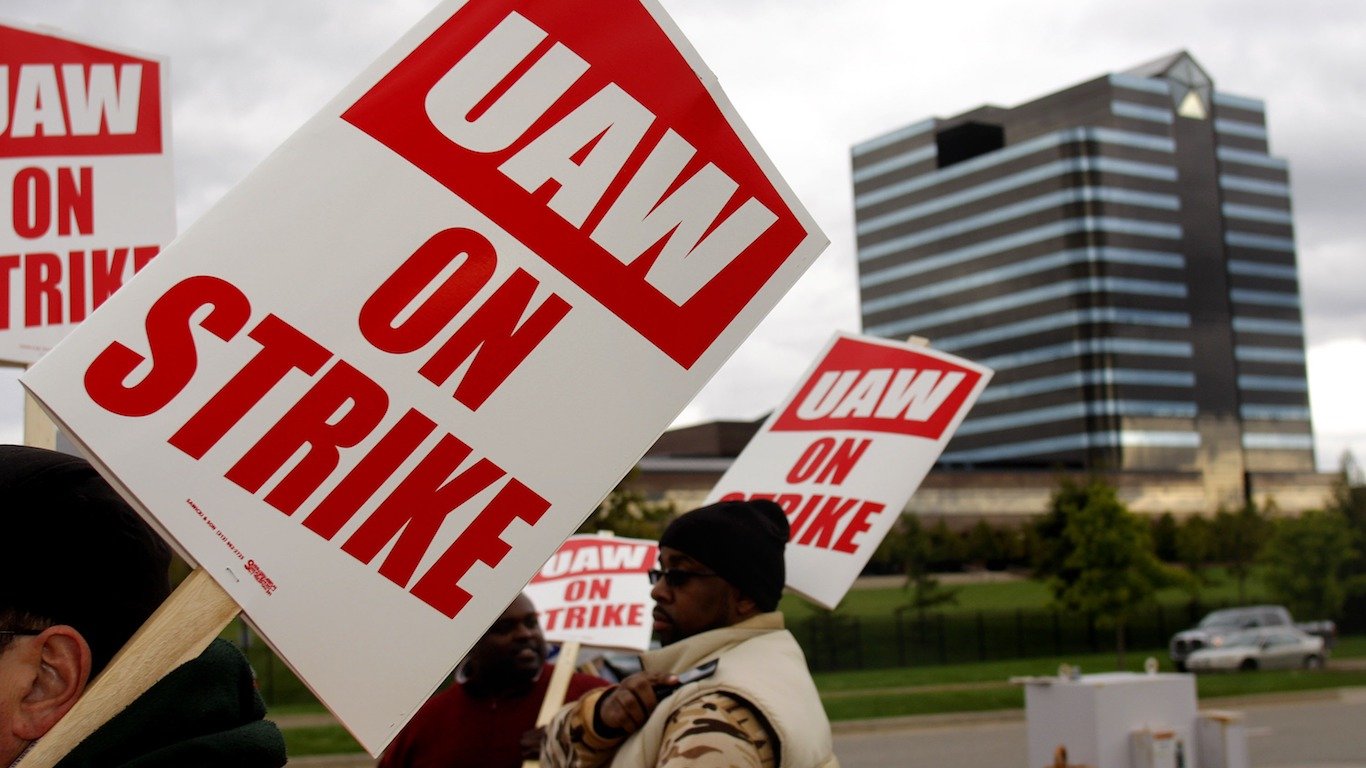

Car prices will almost certainly rise again, and that increase could be sharp. The United Auto Workers (UAW), seeking a rich contract for its 124,000 members, will probably strike GM, Ford and Chrysler’s parent. The car companies may shutter factories rather than give in to a UAW contract that gets their members a 46% pay raise over four years and a work week cut to 32 hours. The contract could permanently damage profitability while these companies pour billions of dollars into developing and producing electric vehicles (EVs).

[nativounit]

Can Americans pay an even higher median price for new cars they buy? For many, the answer is no. Not only are the base prices higher, but they also occur during a period when car loans carry high interest rates. Before the pandemic, many manufacturers offered 0% financing.

[wallst_email_signup]

The alternatives for Americans are to keep their current cars or buy used ones. The average age of a car on the road in the United States is 12 years and rises annually. Used car prices are almost always below new car prices, but these prices also skyrocketed during the pandemic because of low supply.

[recirclink id=1212561]

If a strike goes on for months or even weeks, Americans will pay more for new cars.

Contact [email protected] for any questions or corrections.